Why Millennial Dads Are Quietly Obsessed With Money

The fixation doesn’t arrive with a spreadsheet or a lecture. It shows up in the small things: the nearly compulsive tracking of subscriptions, the way conversations about a birthday become debates over whether to invest the cash instead, the repeated mention of equity versus rent in the same breath as a sleep-training anecdote. For many millennial fathers — roughly those born between 1981 and 1996 — money is a background hum that never quite goes away. It colors how they parent, how they plan for the future, and how they see themselves as providers and partners.

millennial dads financial anxiety

What appears at first to be prudence often looks like obsession: an anxious, detailed attention to financial life that can be both adaptive and corrosive. This is a feature of a generation shaped by repeated economic shocks, shifting labor norms and a social media era that broadcasts both triumph and insecurity. Below, I trace where that fixation comes from, how it manifests in daily life, and what it means for relationships, mental health and policy.

A generation shaped by crisis

Millennial dads carry economic histories that differ sharply from those of older parents. Many entered the workforce at the tail end of the dot-com boom or during the Great Recession of 2007–2009. For a cohort coming of age as housing prices, student debt and healthcare costs soared, the idea of steady upward mobility no longer felt guaranteed. Economic shocks were not distant headlines but life-shaping events.

That context produces habits: frugality where previous generations might spend freely, a skepticism of risk paired with a simultaneous hunger for returns (hence the embrace of investing apps and, for some, crypto), and a persistent sense that every financial choice feels consequential for the children they now raise.

What the fixation looks like

1. Savings as a moral act

For many millennial dads, saving isn’t merely practical — it’s moral. Building an emergency fund, maxing out a retirement account, or opening a 529 plan are gestures that confirm competence and protect children from the fragility they remember from their own adolescence. Conversations about money with friends often center on rates of return, fee drag, and tax-advantaged accounts, not because fathers enjoy the math but because financial security has become a proxy for parental love.

Money becomes the language of responsibility; the more you can quantify, the more you can prove you’re keeping your child safe.

2. Side hustles and identity

Side hustles are not just income supplements; they’re identity projects. Podcasting, consulting, selling vintage clothing online — these undertakings allow fathers to feel proactive in an uncertain labor market. They also blur the line between work and family time: a side gig that starts as a way to pay for childcare may become another pressure point when it consumes time and mental energy.

millennial fathers side hustles

3. Investing as ritual and escape

Investing has become a hobby, a status symbol, and sometimes an escape from the day-to-day anxieties of parenting. The rise of commission-free trading and fractional shares made markets accessible; social media made investing a spectacle. Some millennial dads treat an investing app like a video game — a place to win small victories that feel both practical and symbolic.

millennial dads investing apps

Economic drivers and cultural pressures

Student debt, housing and stagnating wages

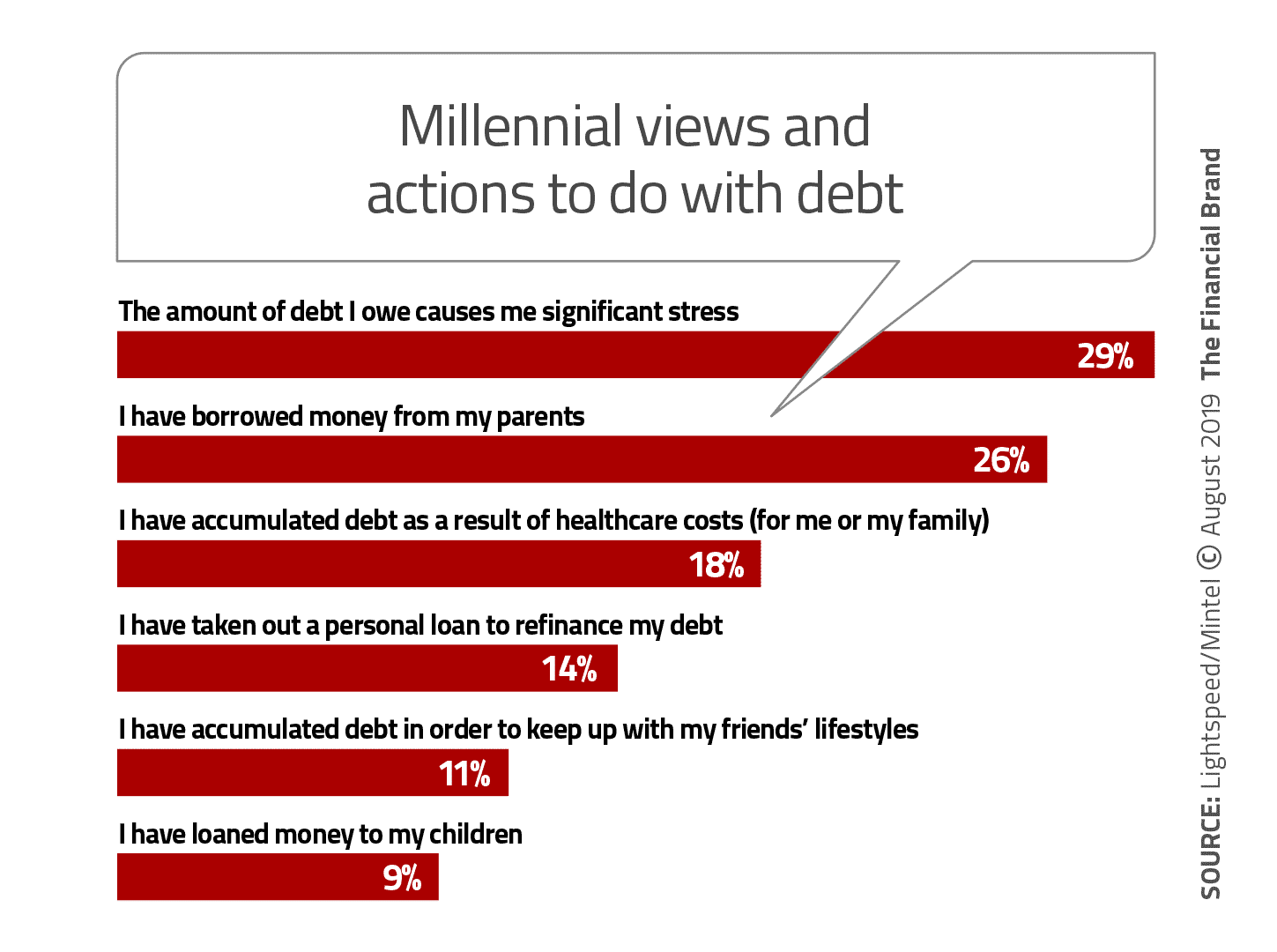

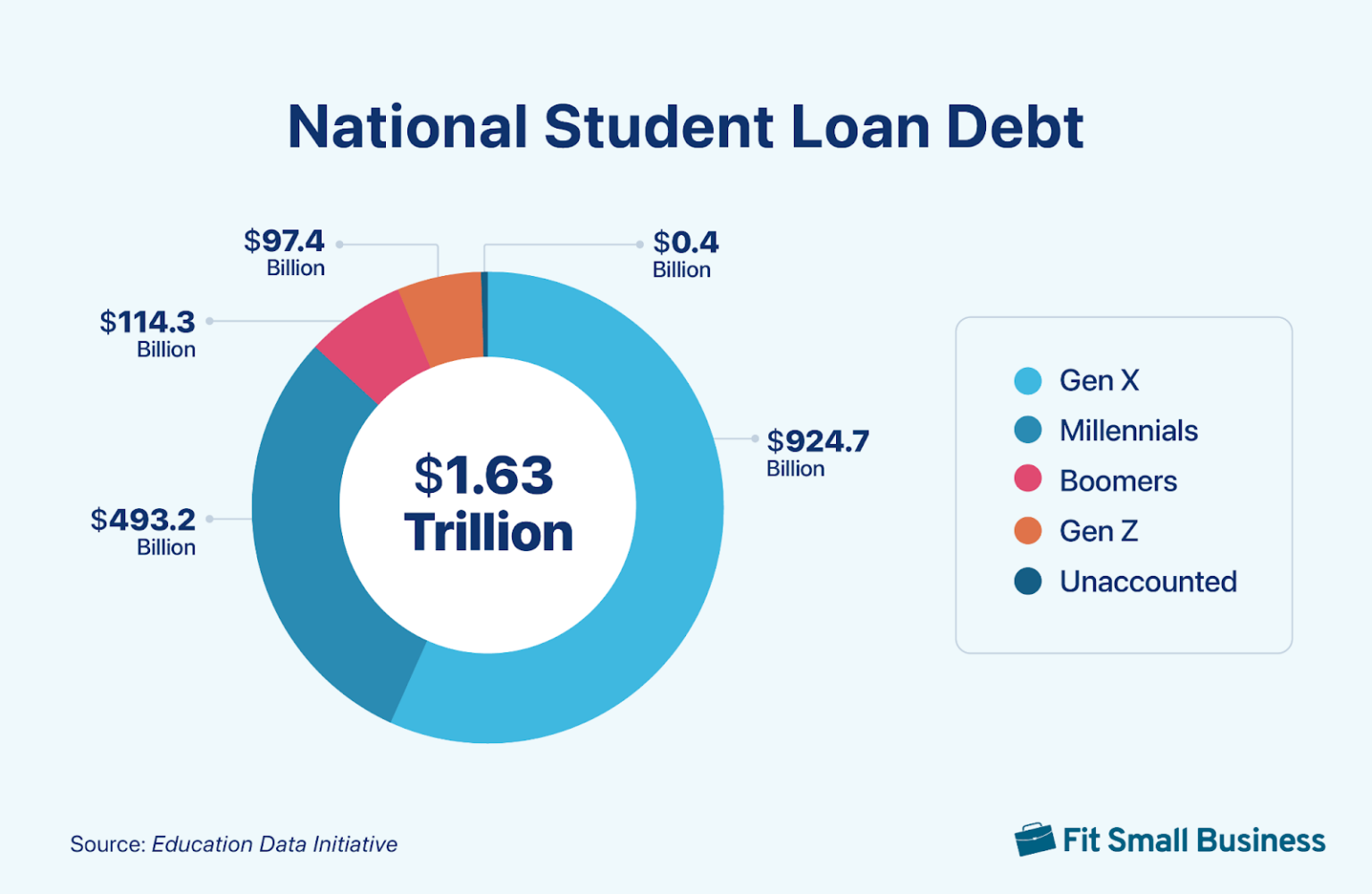

Two realities converge for many: higher costs for housing, education and healthcare, and wages that in many sectors lag behind inflation. Student loan burdens push household budgets into a different shape; rent and down payment barriers delay home ownership or force compromises. For a father attempting to secure stability, those structural pressures translate into hypervigilance about every expense and investment decision.

millennial dads student loan debt

Comparison culture amplified

Social media complicates this further. Platforms curate triumphs and big purchases, normalizing a standard of living that may be unrepresentative. Millennial dads can feel both judged and competitive — an instinct that pushes them toward visible financial moves (a flashy watch, a house in a particular neighborhood) or toward a quieter counterreaction: saving and minimizing to avoid appearing reckless.

It’s not just about how much you have; it’s about how your choices read to other parents.

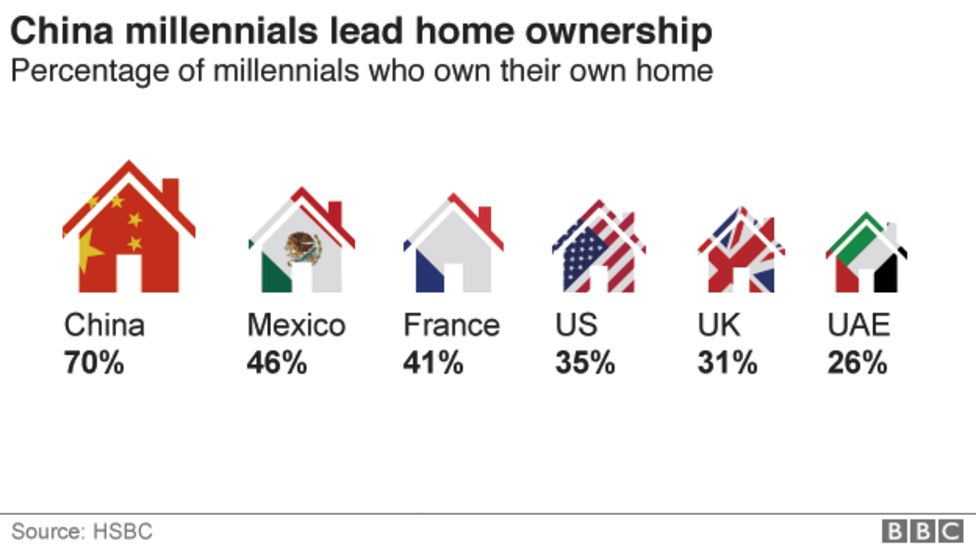

For many, this manifests most acutely around one of the biggest financial decisions: buying a home. The pressure to own, combined with soaring prices, creates a specific kind of fixation.

millennial fathers home ownership

How this affects relationships and parenting

Money talks become emotional labor

In relationships, the fixation on money can mean that financial planning becomes a dominant source of conversation — and conflict. One partner’s thrifty instincts can feel controlling to the other; another’s appetite for risk can feel reckless. For millennial dads, who are often explicitly involved in caregiving in ways older generations were not, money talk is also parenting talk. Every saved dollar is framed as a future opportunity for the child, and that pressure can turn financial prudence into a form of policing.

Mental health under the spreadsheet

Constant vigilance about finances comes with psychological costs. Hyperfocus on future risk increases anxiety and can erode presence in everyday parenting. Some dads report feeling guilty about splurges — even small ones — as if any deviation threatens the family’s safety net. That guilt is linked to perfectionist ideals of fatherhood and the modern expectation to be both a provider and an engaged parent.

Where the fixation helps — and where it hurts

Benefits

- Greater preparedness: More families have emergency funds and retirement plans than previous generations at comparable ages.

- Intentionality: Spending is more often deliberate, with money directed toward education, health and experiences that matter.

- Financial literacy: The average millennial dad is more likely to engage with budgeting tools and financial education resources.

Costs

- Stress and relationship strain: Financial focus can crowd out emotional connection and shared leisure.

- Risk aversion that limits joy: Excessive frugality can reduce experiences for families today in the name of security tomorrow.

- Identity tied to net worth: Self-worth tethered to financial metrics can undermine paternal confidence when markets dip.

- Preparedness for emergencies and education costs.

- Intentional saving for long-term goals.

- Anxiety and diminished present-moment parenting.

- Overcontrol in household spending decisions.

Practical moves for less anxiety, more agency

Being money-conscious is not the problem — being consumed by it is. Here are practical adjustments that preserve the upside while reducing harm.

Create rules, not endless decisions

Set simple rules that automate behavior: automatic transfers to savings, a fixed monthly contribution to college or retirement, and a modest discretionary spending allowance. Rules reduce the cognitive load and the guilt around small purchases.

Reframe goals to include present joy

Deliberately budget for experiences you want to have with your children. Teaching kids values through activities — a modest vacation, a museum trip, a weekend workshop — can be as valuable as a contributed dollar toward a future account.

Share the emotional labor

Money talk is also emotional work. Make space in the relationship for nonjudgmental conversations about fears and priorities, not just spreadsheets. Regular check-ins that combine numbers with values — what matters to us now? — can recalibrate anxiety into teamwork.

Policy and cultural fixes that would help

Many drivers of this fixation are structural. Policies that reduce the precarity of parenting — affordable childcare, higher wages, more flexible parental leave, student debt relief options — would allow more families to move from hypervigilance to stability. Culturally, normalizing financial imperfection and broadening the image of successful fatherhood beyond net worth could relieve private pressure.

Conclusion

The quiet fixation on money among many millennial dads is understandable and in many ways adaptive: a protective response to lived economic instability. It has produced beneficial outcomes — more families are saving and planning — but it also carries costs in stress, relationship tension and diminished presence. The corrective is not telling millennial dads to stop being prudent. It is building environments, both personal and societal, that allow prudence without paralysis.

When financial planning becomes a shared, values-driven practice rather than a solo performance, families gain both security and the space to live. The goal should not be a perfect ledger; it should be a life where money serves parenting, not the other way around.

- Millennial dads' money fixation stems from economic shocks, rising costs, and cultural comparison.

- It yields preparedness and financial literacy but also anxiety and relationship strain.

- Practical strategies — rules, shared conversations, and prioritizing present joy — can reduce harm.

- Policy changes around childcare, wages and debt would ease the structural pressures that feed fixation.

A note on tone: this piece draws on observed trends and common experiences among modern fathers, aiming to explain without judging.