Why $2 Bills Could Be the Ultimate Hedge Against Deflation

The idea sounds almost quaint: a rarely seen two-dollar bill folded into a sock, tucked into a travel wallet, or kept in a home safe as insurance against economic strangeness. Yet beneath the novelty lies a simple reality—during periods when prices fall and the central bank tightens, some forms of cash gain purchasing power in ways that bonds and stocks do not. This piece examines why a $2 bill is more than a curiosity: it is a compact, practical, and psychologically resilient instrument that can play a role in a household or small-business strategy for deflationary risk.

Money that feels scarce can behave like a hedge because scarcity and acceptance determine value as much as face value does.

THE THESIS

The core claim is straightforward: in a deflationary scenario—falling prices combined with monetary tightening—holding physical cash preserves and increases real purchasing power. A $2 bill, because it is physically denser in purchasing power than a $1 bill and culturally scarce, offers a few practical advantages over other denominations for those who prefer tangible hedges. This article unpacks that claim, shows how it fits within broader monetary mechanics, explores real-world logistics, and highlights the limitations and risks of the strategy.

UNDERSTANDING DEFLATION AND THE FED

What deflation looks like

Deflation is not just lower prices—it's a persistent, economy-wide decline in price levels, usually accompanied by falling wages, rising real debt burdens, and caution-driven declines in spending. For individuals, a dollar buys more tomorrow than it did today. For borrowers, debts become harder to service in nominal terms. Central banks like the Federal Reserve respond to deflation with policy tools: cutting interest rates, expanding balance sheets, and deploying unconventional measures. But when those tools are exhausted or when the central bank tightens to defend a currency or price stability, the relative appeal of physical cash rises.

How central bank policy affects cash

When the Fed lowers policy rates, nominal bonds can lose yield and cash becomes comparatively less attractive. Conversely, in a deflationary shock—especially if rates are already low—the real return to holding cash (the implicit return from prices falling) can be positive. Crucially, this is true of any denomination of fiat currency; the argument for $2 bills hinges on logistics, psychology, and small practical benefits rather than any special legal or monetary status.

$2 bill Federal Reserve policy

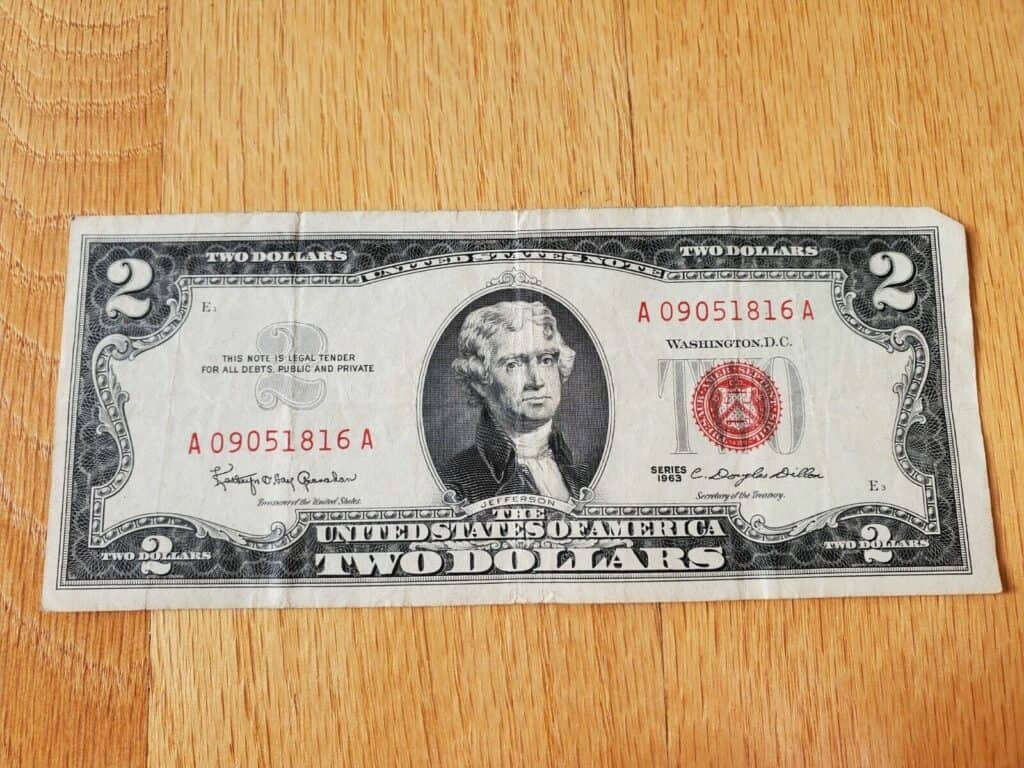

WHY THE $2 BILL?

Less bulk, more purchasing power

One simple arithmetic advantage of the $2 bill: it halves the number of items you need to carry to represent the same nominal holdings compared with $1 bills. In practical terms, if you want to keep $200 in small cash for daily transactions or emergency swaps, 100 $2 bills occupy less volume and weigh less than 200 single-dollar bills. In a world where portability and concealment matter—think emergency stashes or a minimalist traveler's wallet—this matters.

$2 bill legal tender

Scarcity and psychological acceptance

$2 bills are not printed in the same volume or circulated with the same intensity as $1 bills. That scarcity gives them two social effects. First, they feel special—recipients remember receiving one and are more likely to treat it differently. Second, the novelty makes them conversation tools in barter and local exchange during periods where trust in banks dips. The combination of legal-tender status and low circulation means a $2 bill can be both a practical unit of exchange and a memorable token in small peer-to-peer trades or community markets.

$2 bill physical cash

Numismatic upside

Some $2 bills, especially older series or uncirculated specimens, carry collectible value that can outpace inflation or provide an additional premium in trades. This is not guaranteed and should not be the primary reason to hold $2 bills, but the numismatic angle creates a small but useful asymmetric upside for holders who find the right bottlenecks—rare serial numbers, specific series, or crisp notes in uncirculated condition.

$2 bill numismatic value

PRACTICAL APPLICATIONS

Tactical cash reserves

Think of $2 bills as part of a layered cash strategy. If you hold physical currency for emergencies—temporary bank outages, power failures, or the first days of a market shock—$2 bills reduce bulk and increase the odds that recipients will notice and accept them. A suggested approach: keep a mix of denominations (ones for miscellaneous small purchases, twos for compact mid-range needs, fives and tens for higher transactions). The $2 fits the mid-range gap neatly.

$2 bill compact emergency reserve

Barter and small-economy advantage

In localized barter networks or pop-up markets, a $2 bill can be an easy, memorable denomination that simplifies trades. Sellers often prefer rounder numbers or denominations they can give change from; a $2 bill requires less change for common small purchases (two-dollar coffee, small street food items, a modest bus fare—examples vary by region) and can become a favored unit for repeat transactions.

$2 bill barter advantage

RISKS, LIMITS, AND MISCONCEPTIONS

Not a sovereign store of value

Important caveat: a $2 bill is still fiat currency. It does not have intrinsic value like gold or a guaranteed yield like bonds. In hyperinflationary scenarios the logic flips—paper money loses value rapidly and small-denomination bills become worthless for larger purchases. The $2 bill's hedge value is specifically tied to deflationary or liquidity-risk scenarios where cash's purchasing power rises or remains stable relative to financial assets.

Acceptance and merchant behavior

While $2 bills are legal tender, many merchants are unfamiliar with them. That can slow transactions or create confusion, especially in automated systems designed around more common denominations. For frequent or bulk transactions, $2 bills are not a substitute for bank deposits or digital payment rails. Their utility is greater in person-to-person exchanges or as a discreet physical reserve.

A PRACTICAL CHECKLIST

How to assemble a $2-bill component of your emergency cash

- Amount: Decide on a target level—enough to cover 1–2 weeks of essential cash expenses in a worst-case scenario.

- Denomination mix: Keep 10–30% of that target in $2 bills to reduce bulk; complement with $1, $5, and a couple of $10 or $20 bills for larger payments.

- Storage: Use a fireproof safe or hidden emergency envelope; rotate notes every few years to keep paper fresh.

- Accessibility: Keep part of the stash truly accessible (in a wallet or travel pouch) and part locked away for contingency.

COMPARISON TABLE

Denomination trade-offs at a glance

| Denomination | Bulk for $200 | Merchant Familiarity | Use Case |

|---|---|---|---|

| $1 | 200 bills | Very high | Everyday small purchases |

| $2 | 100 bills | Moderate | Compact mid-range cash reserve |

| $5–$20 | 40–10 bills | Very high | Larger purchases, change-making |

PSYCHOLOGY AND SOCIAL DYNAMICS

Money is not purely arithmetic; social perception matters. A $2 bill handed in a tense situation—imagine a line at a farmer's market following a temporary outage—can be more noticeable and therefore more likely to be accepted than a stack of ones. Collectability also colors behavior: people sometimes give a $2 bill as a tip or a token, increasing the chances the bill circulates among networks that value it. That social velocity can be an advantage when trust in digital rails declines.

WHEN IT WORKS BEST

Scenarios where a $2-focused tactic is sensible include short-to-medium length deflationary episodes, localized liquidity disruptions, and contexts where portability and discretion matter. It is less useful in long-term inflationary collapse, in fully digital economies where cash is impractical, or in transactions requiring large purchases where higher denominations or digital funds are more convenient.

PROS AND CONS

- Compact — more purchasing power per bill than $1s.

- Memorable — psychological advantage in peer trades.

- Legal tender — accepted by law across the country.

- Numismatic potential — select notes can carry premiums.

- Limited liquidity — some merchants unfamiliar or automated systems incompatible.

- Fiat risk — loses value in inflationary crises.

- Storage risks — theft, loss, and deterioration.

IMPLEMENTATION AND MAINTENANCE

Sourcing $2 bills

Most banks will exchange bills on request from their cash stock; however, public circulation is limited so patience and polite requests help. A practical route is to ask your teller for several $2 bills over multiple visits or request them when withdrawing a round sum. For collectors seeking particular series or uncirculated bills, specialty dealers and reputable auctions are appropriate, but that crosses from practical hedging into numismatic collecting.

Rotation and record-keeping

Rotate your cash reserves every few years to avoid excessive wear that makes notes less acceptable. Keep a simple, secure record of serial numbers only if you hold particularly rare notes; otherwise, treat these bills like any other cash reserve. If you contribute to community barter pools, document the amounts you place and the recipients to maintain trust and avoid disputes.

CONCLUSION — A SMALL DENOMINATION WITH BIG IMPLICATIONS

The $2 bill is not a magic bullet. It will not replace diversified asset allocation, insurance, or prudent household budgeting. What it offers—compactness, novelty-driven acceptance, modest numismatic upside, and straightforward legal-tender status—makes it a surprising and sometimes useful complement in a defensive cash toolkit aimed at deflationary or liquidity-risk scenarios. For people who value physical, portable, and psychologically effective forms of emergency money, a chunk of $2 bills is cheap insurance and a practical hedge.

- During deflation, physical cash gains real purchasing power—$2 bills make that cash more compact and memorable.

- $2 bills are legal tender and practical for short-to-medium emergency reserves but are risky as a lone hedge against broader macro risks.

- Use $2 bills as part of a diversified cash and asset strategy; rotate and store them securely.