When Tailors Make Money: Somalia's Hand‑Stitched Currency

On a humid morning in a market alley of an unnamed Somali city, a narrow shop glows beneath a faded awning. Inside, the rhythmic staccato of a sewing machine punctuates bargaining voices. The tailor at the bench is not only mending shirts; he is sewing what the neighborhood accepts as buying power: small, hand-stitched cloth notes, carefully numbered and signed, passed from merchant to merchant like a circulating promise. For regulars, the fabric slips into wallets next to banknotes and mobile receipts. For visitors, the sight is startling — a grassroots answer to a deeper breakdown in formal money issuance and public trust.

Somali tailor sewing machine

“Money is not only paper or metal; it is permission and promise,” a trader explains, holding a square of cloth with a stitched emblem. “We made our own permission.”

How Did Paper Give Way to Thread?

The headline image — a central bank that no longer prints currency and tailors stepping into the breach — reads like allegory. In reality, the shift toward locally produced scrip in parts of Somalia is less sudden theatre than a slow coagulation of necessity, history and improvisation. Decades of political fragmentation, disruptions to formal institutions, and the high cost or insecurity of transporting printed banknotes created an environment in which communities sought stable, trusted alternatives.

Somalia central bank building

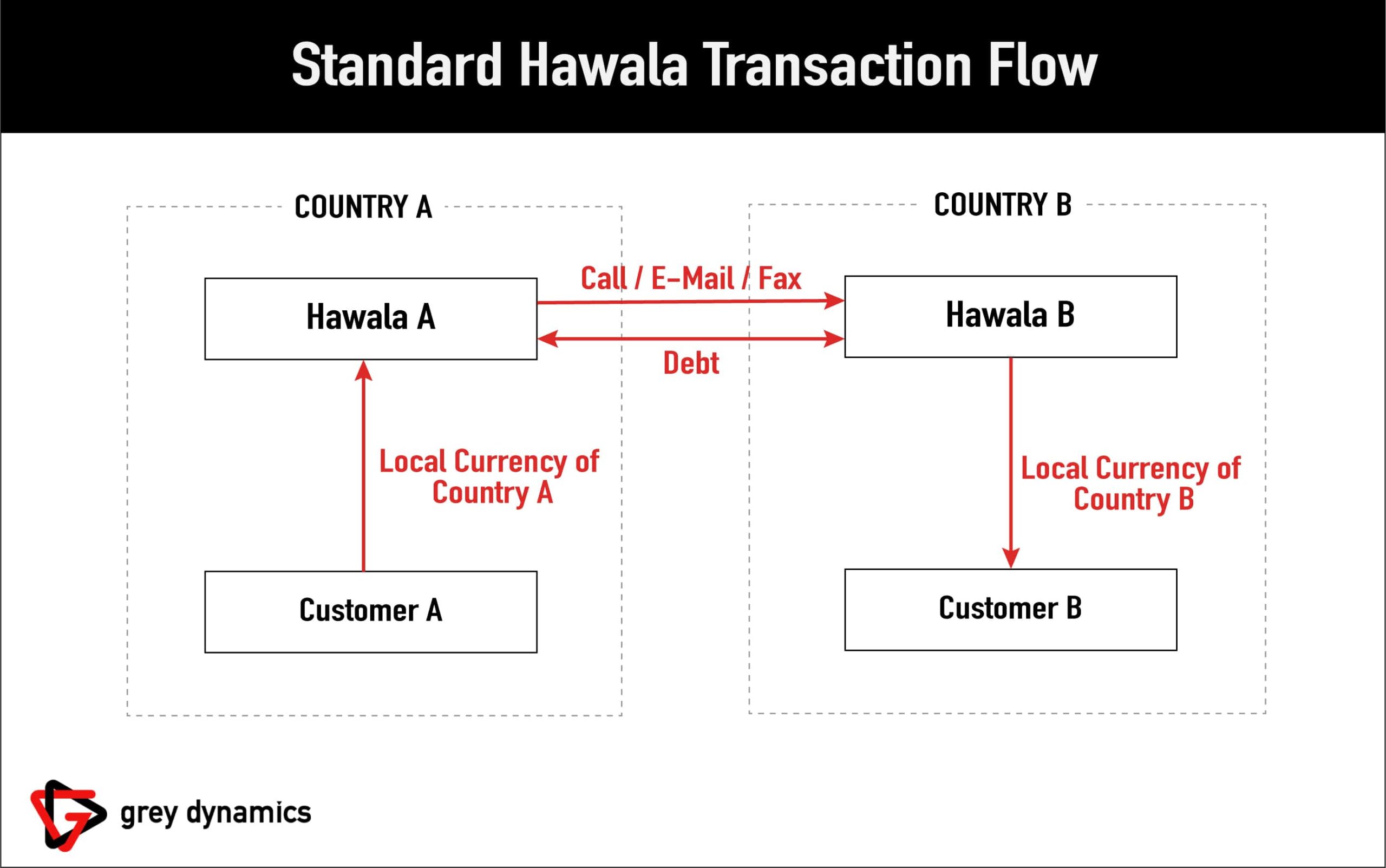

When formal channels for currency distribution are interrupted, trust does the heavy lifting. Trust curves across families, shopkeepers, remittance corridors and mobile-money operators. In many neighborhoods, that trust is embodied in people — elders, shopkeepers, and yes, tailors — who become guarantors. The tailor’s sewing machine becomes a compact printing press: a way to issue tokens that represent value in a specific market or network.

A closer look: The mechanics of hand‑stitched money

What the cloth notes are

Hand-stitched notes vary widely. Some are strips of used fabric with inked or embroidered denominations and merchant stamps. Others are more elaborate: layered fabric with sewn serial numbers, a merchant's mark, and a ledger entry kept by the issuing artisan or cooperative. They function in practice as vouchers, IOUs, or community scrip redeemable at participating shops or against goods and services provided by the issuer.

Hand stitched cloth notes

Issuance and acceptance

Issuers tend to be trusted local businesses or informal cooperatives rather than lone tailors working in isolation. A group of tailors might form a rotating trust fund, issuing a limited run of cloth notes backed by their combined stock of goods or future services. Acceptance depends on social network density: the more merchants that sign on, the more liquid the scrip becomes. Acceptance is often reinforced by visible marks — embroidered designs, stamps, or signatures — that are hard for casual counterfeiters to reproduce.

Why tailors? The intersection of craft, credibility, and commerce

Tailors occupy a distinctive social and economic position in many Somali communities. They are artisans who handle materials, maintain visible shops in marketplaces, and regularly interact with customers across social strata. They keep ledgers, charge for bespoke services, and often operate on credit terms with clients. These attributes make tailors natural candidates to underwrite community money.

Technically, a tailor's kit can also deter simple counterfeiting: threads, unique stitch patterns, and localized dyes create a tactile authentication system that a photocopier cannot replicate. More importantly, tailors are readable symbols of continuity: a tailor who has stitched suits for generations stands as a living guarantor of a note's acceptability.

Textile artisan embroidery Somalia

Everyday life with stitched notes

Imagine buying bread with a small square of indigo cloth, or paying for taxi fare with a sewn slip that a barber will accept for a haircut next week. Stitched notes coexist with hard currency and mobile transfers. They reduce friction for routine transactions when small denominations of official currency are scarce. For shopkeepers, they offer a means to extend short-term credit tied to local reputation rather than bank collateral.

Somali market merchants trading

A temporary bridge, often

In many cases, these instruments are explicitly understood as stopgaps. Merchants calculate their exposure: how many cloth notes are in circulation, which issuers are reliable, and how quickly the network can convert scrip back into goods, services or formal cash. Where remittance flows or mobile-money liquidity improve, the cloth notes often recede.

Hawala money transfer Somalia

Economic implications: More than a quaint workaround

At first glance, hand-stitched currency looks like folkloric ingenuity. But its presence carries measurable economic effects.

- Liquidity smoothing: Scrip eases everyday transactions when small denominations are scarce, preventing barter or market stalls from shuttering.

- Credit extension: Because many notes act as merchant IOUs, they extend informal credit to customers who lack access to banks.

- Local multiplier: Money that circulates within a tight network tends to have a higher local multiplier, keeping purchasing power in the community.

These benefits come with risks: limited convertibility, uneven acceptance, inflationary pressure within the micro-economy if too much scrip is issued, and the potential erosion of broader monetary control if large networks start to set their own rules.

Risks, governance and counterfeit threats

Counterfeiting and dilution

Every issuer depends on scarcity and credibility. If anyone can sew a facsimile, the system degrades. Communities counter this through informal governance: public shaming, refusal of suspicious notes, or coordinated boycotts of rogue issuers. Those measures work in dense social networks but weaken as economic actors become more anonymous.

Monetary policy blind spots

Local scrip poses a challenge for macroeconomic policy when it scales. Central banks manage inflation and liquidity by controlling the money supply. When large portions of transactional value slip into informal instruments beyond the central authority's view, monitoring and intervention become harder. In fragile states, policymakers must weigh the immediate market-stabilizing benefits of scrip against longer-term risks to fiscal and monetary coherence.

Cultural and symbolic dimensions

Money is cultural as much as it is economic. The choice to sew instead of print embeds value in craft. Embroidered motifs reference clan marks, local motifs and religious inscriptions; the tactile texture of cloth carries history and identity. For many participants, using a tailor-made note signals community belonging as much as it enables trade.

Stories stitched into fabric

One small shopkeeper described keeping a particular stitched note wrapped in a drawer because it bore the mark of a deceased generator of the community's trust. The item acted like a relic — a reminder that money in that network was not neutral but a repository of personal histories and relationships.

Could hand‑stitched money become formalized?

There are plausible pathways to formalization without losing the benefits of local trust. Cooperative structures could register their scrip, agree to limited issuance, and open transparent ledgers that allow conversion to formal currency on agreed terms. Mobile platforms — already widespread in Somalia's remittance-rich economy — could electronically encode scrip balances, allowing issuers to maintain control while expanding acceptance.

Design principles for safe formalization

Practical policies would include: caps on issuance backed by pledged goods or services; simple authentication features tied to local artisanship; community-level dispute resolution mechanisms; and interoperability agreements with remittance and mobile-money operators. Importantly, any formalization must preserve the trust banks cannot buy: local credibility.

Lessons for fragile states and policymakers

The Somali experience — where tailoring shops double as micro-issuers of value — offers broader lessons. When institutions falter, communities improvise. That improvisation is not purely reactionary; it reveals durable design principles for inclusive money systems: proximity, transparency, limited issuance, and social enforcement.

Policymakers and development practitioners should treat such systems as data-rich laboratories rather than curiosities. Studying when local scrip stabilizes trade versus when it fragments marketplaces can guide interventions that strengthen resilience without crushing local agency.

What this means for the future of money

Hand-stitched notes in Somalia are a potent reminder that money is fundamentally a social technology. In an era of digital payments and central bank digital currency (CBDC) experiments around the world, the grassroots emergence of textile scrip shows the limits of technology divorced from trust. Digital records are powerful, but they cannot by themselves substitute for local legitimacy.

At the same time, hybrid solutions can combine the best of both worlds: artisan-backed tokens with mobile redemption rails, or community-issued credits recorded on simple interoperable platforms. Such models could expand financial inclusion where banks do not reach and offer a measured way to rebuild links between communities and formal institutions.

Conclusion

The image of tailors printing money with needles and thread serves as both metaphor and reality. It captures how communities invent practical solutions under strain and how meaning, craftsmanship and credibility can become currency in their own right. For traders and tailors, the cloth note is a working tool for daily life; for observers it is a living lesson about what money really is: an agreement to accept value from strangers because of people you trust.

“When institutions are thin, people thicken them with relationships,” a market elder reflects. “That is how trade survives.”

- In contexts of institutional weakness, communities may create locally issued scrip to maintain daily trade.

- Tailors and artisans can serve as credible issuers because of visibility, reputation, and technical uniqueness.

- Such systems offer liquidity and local credit but carry risks of dilution, limited convertibility, and governance failures.

- Formalization is possible through cooperative governance, issuance caps, and interoperability with mobile money, preserving local trust while improving safety.

Final thought

Whether stitched in cloth or encoded in bytes, money depends on stories we tell about trust and value. Somalia's hand-stitched notes are an eloquent chapter in that story — a reminder that when the machinery of states falters, human ingenuity weaves new seams.