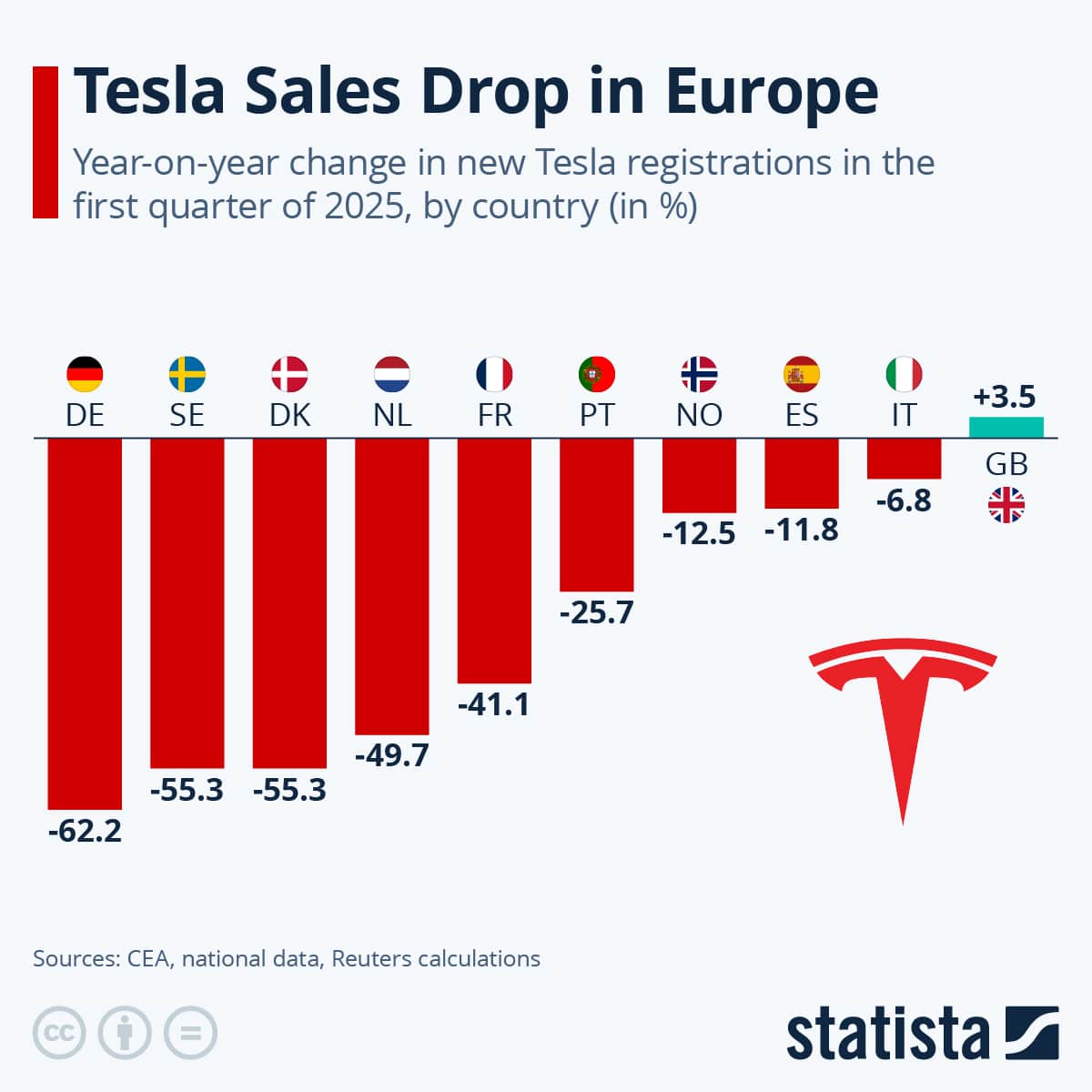

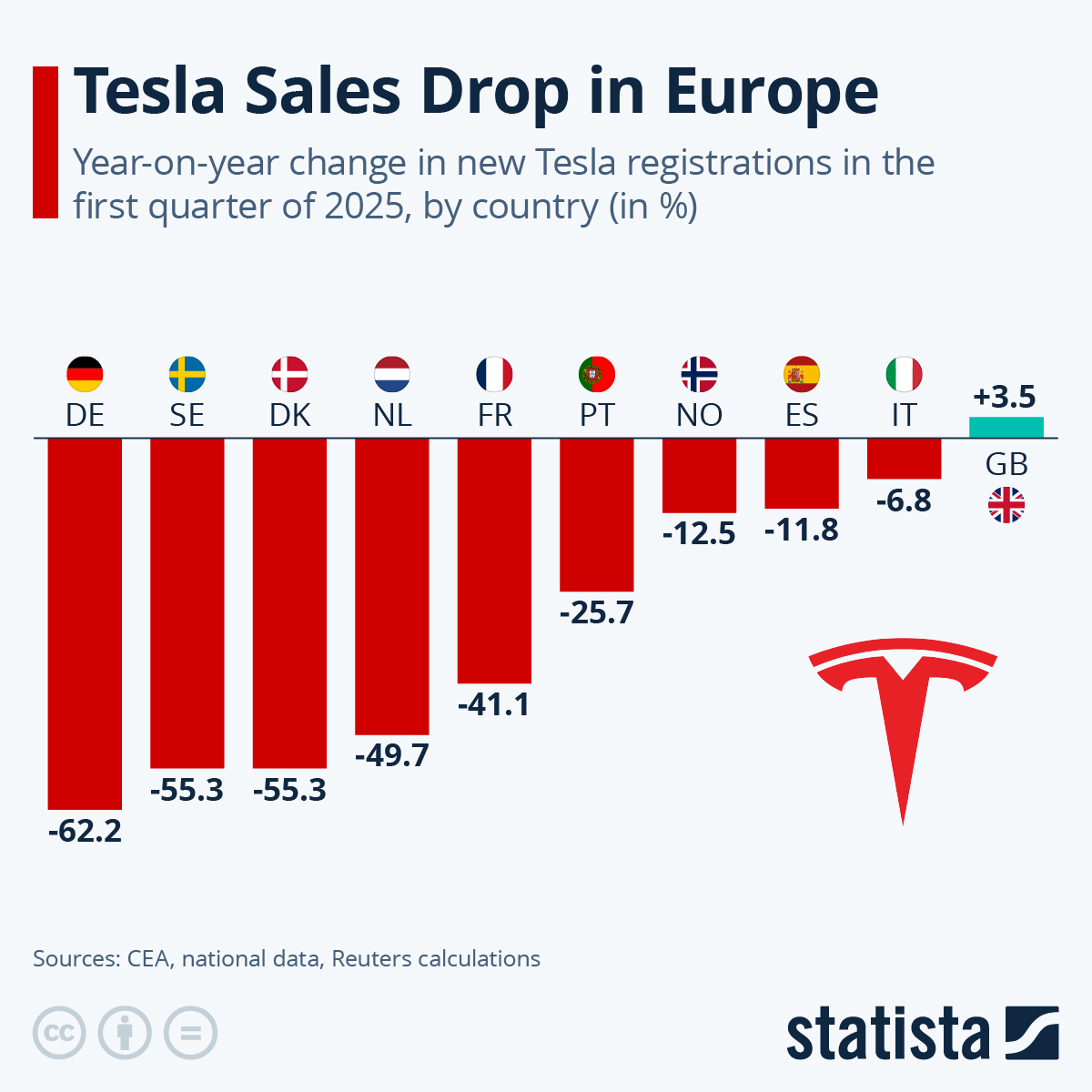

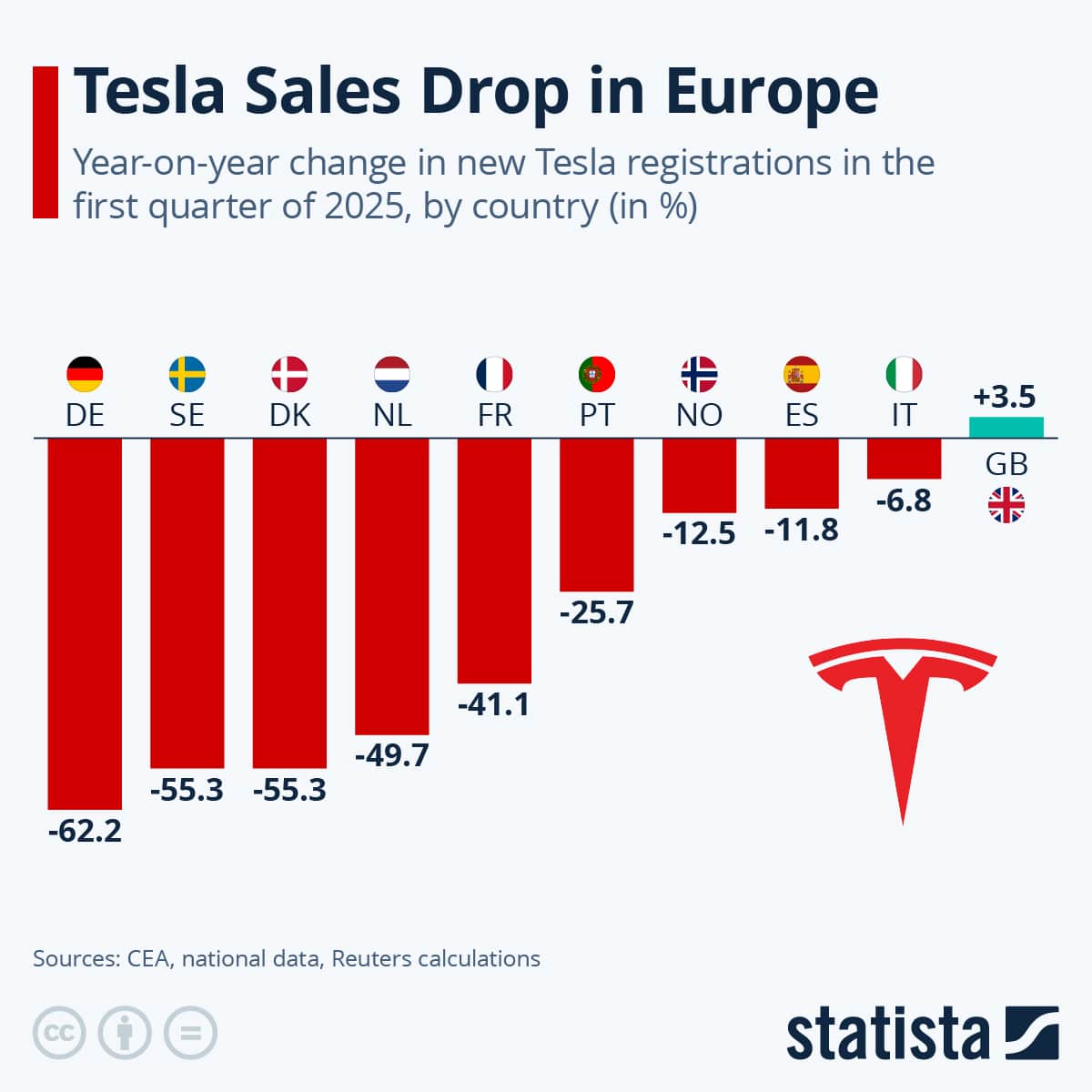

Tesla Sales Plummet in Europe: Sharp Year-on-Year Declines

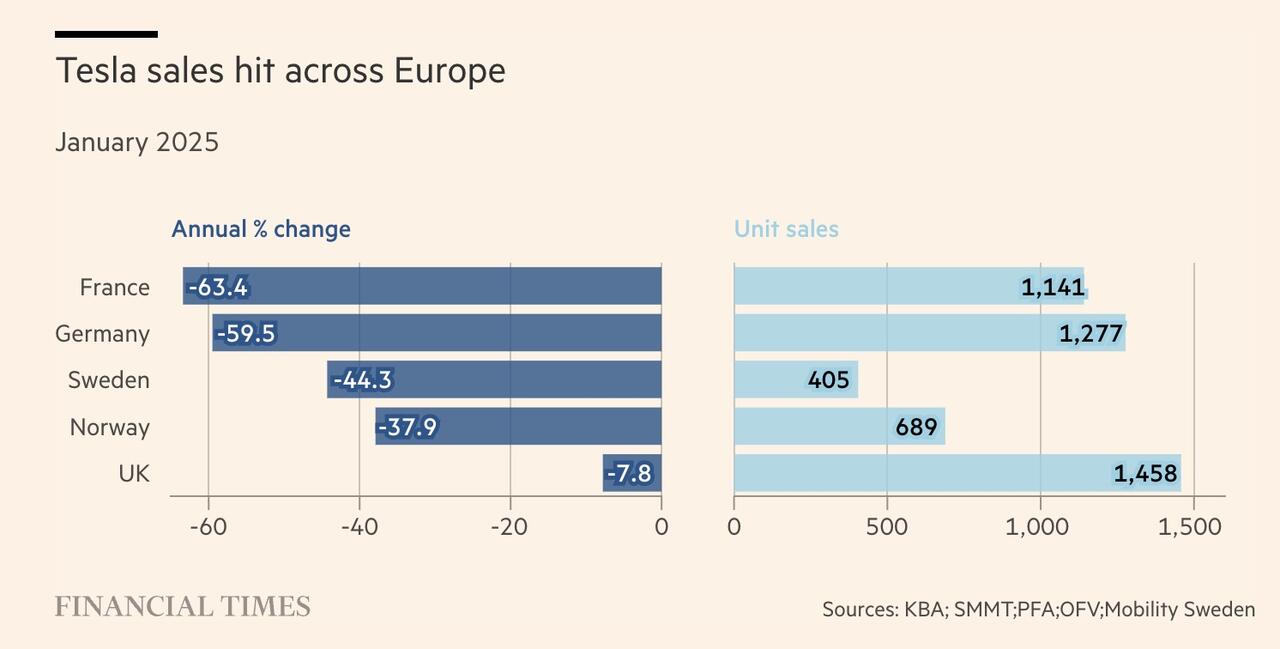

The headline numbers are stark: Tesla sales down by roughly 55% in the United Kingdom, 58% in Spain, 59% in Germany, 81% in the Netherlands and 93% in Norway compared with the prior year. Those percentages alone demand attention — but raw declines are only the start of the story. Behind them are shifting consumer incentives, changing market dynamics, intense competition from established automakers, inventory and pricing strategies, and wider macroeconomic and policy influences that together are reshaping the European electric vehicle market.

UK Tesla sales drop

The real question is not just how much Tesla's deliveries fell, but why Europe — the continent that once embraced EVs fastest — is moving so quickly beneath its feet.

Anatomy of the Decline

High-percentage declines look dramatic, and they are. But percentages can amplify small bases and local quirks: Norway, for instance, has one of the highest EV penetration rates worldwide, which can make year-on-year swings especially volatile as early-adopter demand stabilizes. Still, seeing drops above 50% across major markets like the UK and Germany is meaningful regardless of base effects. These are two of Europe’s largest auto markets and central battlegrounds for EV share gains.

Understanding the numbers

Several technical factors affect reported sales figures: the timing of registrations (quarterly spikes versus steady deliveries), whether exports or fleet sales are included in national tallies, and how manufacturer reporting methods differ across jurisdictions. Beyond methodology, the headline declines likely reflect a mix of reduced consumer demand for Tesla models at previous price points, the knock-on effects of strategic price cuts in prior periods, and the near-simultaneous emergence of compelling alternatives from legacy European and Asian manufacturers.

Country-by-Country: What the Drops Mean

United Kingdom

In the UK, a 55% drop signals more than a temporary lull. British buyers face a different incentive landscape than continental Europe — purchase incentives are smaller, charging infrastructure varies regionally, and the residual values of EVs hinge on a robust used-car market. The UK is also a market where brand loyalty and dealership networks still influence buyers. Tesla's direct-sales model and reliance on online purchasing may restrict impulse buys that dealership displays and test drives traditionally catalyze.

Spain Tesla sales decline

Spain

Spain’s roughly 58% decline points to an EV transition still unevenly distributed geographically. Urban centers such as Madrid and Barcelona see rapid EV uptake, but national uptake is constrained by variable incentives and charging rollout. Spanish consumers are price-sensitive; competition from relatively affordable EVs and plug-in hybrids from local and Asian producers likely undercut Tesla’s market positioning.

Germany Tesla sales fall

Germany

Germany, with a 59% drop, is the most telling. The home of Volkswagen, BMW and Mercedes-Benz is where legacy manufacturers have aggressively pivoted to EVs, often leveraging extensive dealership networks, financing offers, and brand trust. German buyers may be trading Tesla for locally made models that better reflect the country’s expectations on build quality, interior finish, and driving dynamics. Additionally, policy adjustments and fluctuating incentives across federal and state levels can reshape short-term demand.

Netherlands Tesla sales

Netherlands

An 81% decline in the Netherlands is dramatic but must be read in context. The Dutch market was an early adopter of EV incentives and fleet electrification programs; when those incentives change or fleet procurement patterns shift, registration numbers can fall precipitously. Moreover, the Netherlands has seen a proliferation of competitive, lower-cost EVs that meet the needs of urban commuters.

Norway Tesla sales decline

Norway

Norway's 93% drop is the most eye-catching. Norway went from early adoption to mainstream EV dominance faster than any country, largely thanks to generous incentives and a culture that rapidly accepted electric cars. But with near-saturation in prime segments and an older wave of Tesla buyers looking to trade down or delays purchases, registration volatility can be extreme. High previous-year numbers also make declines look larger by comparison.

Root Causes: Demand, Competition and Price Dynamics

Several overlapping drivers likely explain the declines:

- Intense competition: European automakers have introduced a wave of well-priced, well-finished EVs tailored to local tastes. This includes compact crossovers and mainstream family cars that directly compete with Tesla’s entry models.

- Price normalization: Tesla’s earlier pricing strategies — aggressive global price cuts to boost volume — may have rebalanced consumer expectations and dealer pricing across the industry. When price reductions accelerate, some buyers delay purchases in anticipation of further cuts, while others pivot to new releases from competitors.

- Incentive changes: Government subsidies, tax breaks, and registration perks drive EV adoption. Where incentives decline or are restructured, short-term registration numbers often follow.

- Used EV market growth: A larger, healthier used market reduces urgency for new purchases. Buyers can find late-model EVs at meaningful discounts, dampening demand for new vehicles from any brand.

- Model cycle timing: Tesla’s product refresh cadence and availability windows influence sales. Delays or limited local inventory in a given quarter can create headline declines even if long-term demand remains strong.

Tesla Model 3 Europe

Macro and Consumer Sentiment

Economics matters. Inflation, mortgage pressures, and the rising cost of living affect discretionary purchases, including higher trim and longer-range EV variants. In many European countries consumers are more sensitive to upfront cost than to total cost of ownership calculations favored in the U.S. That cultural difference benefits manufacturers that offer compelling financing and trade-in deals through established dealer networks.

Tesla Model Y Europe

Tesla Strategy: What May Be Behind the Numbers

Tesla’s global playbook has emphasized scale, vertical integration and direct engagement with customers. But the Europe challenge reveals friction points: logistics of delivering cars across multiple countries, localized regulatory environments for safety and software, and service network density that lags behind dealers with decades-long footprints.

Pricing and inventory tactics

To defend margins, Tesla has oscillated between price cuts and localized incentives. Those moves can temporarily boost volume, then create soft months as the market recalibrates. Inventory buildup can also prompt temporary registration slowdowns — dealers and distribution hubs may delay national registrations while optimizing allocations.

Service and delivery experience

Customer experience remains a differentiator. Slow service appointment availability, regional parts constraints, or limited test-drive opportunities can nudge buyers toward OEMs that offer immediate demonstrations, flexible financing and established after-sales support.

Competitive Landscape and Model Mix

Legacy automakers have launched a torrent of purpose-built EVs that cater to European tastes: compact crossovers, premium estate cars, and small city EVs that are cheaper to run and easier to park. Many of these rivals benefit from established manufacturing footprints inside Europe, which reduces delivery times and enhances residual-value confidence among buyers.

European EV competition

What consumers are choosing instead

European buyers increasingly value practical range, interior comfort, and traditional brand cues. Some competitors also match or exceed Tesla on software and connectivity as automakers abandon the idea that Tesla owns the “software-first” crown. Add strong dealer financing and familiar service touchpoints, and the competitive advantage narrows.

Competition is no longer hypothetical. It has arrived with models that check the same boxes — often at lower effective prices when financing and trade-in programs are considered.

Implications for the Broader EV Transition

Short-term sales volatility in any brand does not negate the broader transition to electrified mobility. Rather, it may accelerate consumer sophistication: buyers weigh total cost of ownership, brand experience, charging convenience and resale value with greater nuance. For policy makers, these shifts underline the importance of stable incentive frameworks and charging investment to sustain adoption momentum.

Supply chain and manufacturing effects

Lower new-vehicle volume affects production planning and parts suppliers. If Tesla’s orders into European factories fall, suppliers that ramped to meet previous demand will face pressure to retool or reduce output. Conversely, manufacturers expanding local production can capture market share more rapidly if they maintain steady supply chains.

What Investors and Analysts Should Watch

Short-term registration falls spur headlines, but investors should track leading indicators: order banks, delivery backlog, localized pricing trends, and incentive changes. Listen for signs that declines are structural versus cyclical — are deliveries dropping because of a one-off inventory rebalancing, or because consumers now prefer alternatives?

- Order bank vs. deliveries: A healthy order bank suggests demand will rebound when inventories normalize.

- Pricing trajectory: Continued price competition indicates margin pressure; stabilization suggests a new price equilibrium.

- Incentive announcements: New subsidies or revamps to EV tax treatment can quickly revive demand.

- Service capacity: Expansion of service centers and faster appointment availability improves buying confidence.

What Consumers Should Consider

If you are an intending EV buyer in Europe, these market shifts create opportunities: better negotiating power on price, an expanding range of models to choose from, and a more mature used market. But also weigh long-term support, software update policies, and charging access when comparing offers.

- More choice as legacy automakers introduce compelling EVs.

- Better deals during periods of price competition and inventory correction.

- Stronger used market lowers effective cost of ownership.

- After-sales complexity if service networks are thin in your area.

- Uncertain residuals as market prices find a new equilibrium.

- Potential software fragmentation between manufacturers.

Conclusion: A Market in Transition, Not a Collapse

The numbers — dramatic as they are — are best read as a market recalibrating. Tesla’s sharp year-on-year drops in several European countries highlight a more competitive landscape, changing incentive frameworks, and the maturation of EV demand. For Tesla, the task is to adapt price and distribution strategies to local preferences while strengthening service networks. For competitors, it is an opportunity to convert brand trust and dealer relationships into long-term EV sales.

- High-percentage declines reflect a combination of base effects, incentives, pricing tactics and competition, not necessarily a structural end to Tesla’s European presence.

- Germany and the UK are pivotal: shifts there influence broader continental dynamics.

- Watch order banks, pricing patterns and policy changes to distinguish cyclical dips from structural market share loss.

Final Thoughts

Tesla remains a major force in the EV transition, but the era of comfortable market dominance in Europe is over. As consumers get savvier and rivals sharpen their offerings, market share will become a fight decided by product fit, local execution and the ability to deliver consistent, high-quality customer experiences. The coming year will tell whether these declines were a reset or the start of a longer shift toward a more diversified European EV market.

Analysis and reporting aim to clarify market trends; readers should consider local incentives and dealer offers when making purchasing decisions.