Strait of Hormuz Blockade: Global Trade, Oil, and Shipping Risks

The Strait of Hormuz is a narrow stretch of water that, in global economic terms, functions like a massive valve on the world’s supply chain. A blockage there—whether temporary or prolonged—reverberates far beyond the Persian Gulf. It can push oil and gas prices higher, reroute container and tanker traffic across longer seas, raise insurance premiums, and force companies and governments to make urgent strategic decisions. In this feature I walk through why the strait matters, what immediate and secondary effects a blockade would produce, who pays the price, and how policy makers and private-sector leaders should plan for and respond to disruption.

Strait of Hormuz map

Why the Strait of Hormuz Matters

At its narrowest, the Strait of Hormuz is roughly 21 nautical miles wide, a tight corridor connecting the Persian Gulf to the Gulf of Oman and the Arabian Sea. Despite its modest geography, the passage handles an outsized share of global energy flows: a large proportion of the world’s seaborne crude oil and liquefied natural gas (LNG) passes through this corridor en route to Asia, Europe, and beyond. Shipping lanes and traffic separation schemes concentrate vessel movements; tankers, container ships, and bulk carriers follow predictable tracks that make the strait highly efficient—and, crucially, highly vulnerable.

Iran coastline Persian Gulf

Oil tankers Hormuz

Immediate Market Effects

When a chokepoint like Hormuz is obstructed the most visible result is market volatility. Oil benchmarks respond almost instantly because traders price in two things: the volume of physical supply at risk and the uncertainty about duration. Even a short-lived closure can cause a spike in crude futures and prompt national strategic petroleum reserves to be considered as a stabilizing tool. The same logic applies to refined products and LNG: buyers facing tighter supply windows will bid more aggressively, and regional shortages can emerge quickly.

War-risk insurance maritime

A blocked strait is not just a regional event; it becomes a contest between speed, storage, and market psychology.

Ripple Effects Along Supply Chains

Beyond energy markets, the economic impact travels down complex supply chains. Containerized cargo and bulk commodities that normally transit through the Arabian Sea or via Suez can face longer voyages, delayed transits, and capacity squeezes. For industries reliant on just-in-time manufacturing—automotive, electronics, and certain consumer goods—delays translate directly into production slowdowns. For retailers, inventory backlogs may become acute ahead of seasonal sales windows. Freight rates can spike as carriers reprice risk and add fuel and war-risk surcharges.

Rerouting: Costs, Time, and Practical Limits

When the direct path is blocked, shippers have options but none are cost-free. The most obvious alternates are longer sea routes: vessels can sail around the Arabian Peninsula via the Cape of Good Hope, adding thousands of nautical miles and several weeks of transit time. For container shipping this is possible but expensive—fuel, crew costs, and opportunity costs for vessel utilization all rise. For tankers, longer voyages increase insurance exposure and capital tied up in transit. Pipeline alternatives exist only for onshore transfers—pipelines in the region and across neighbouring countries can shift flows, but they lack the capacity to fully substitute for seaborne volumes and require complex political approvals to increase throughput.

Cape of Good Hope shipping

Insurance, Risk Premiums, and Shipping Practices

Maritime insurance is a market signal. In times of heightened geopolitical risk, insurance underwriters impose additional premiums or 'war risk' cover. These surcharges, passed along by carriers, hit consumers and industrial buyers. Shipping companies may impose 'risk surcharges' or temporarily refuse to call at certain ports. Meanwhile, owners and operators deploy mitigation tactics: sailing with naval escorts when available, implementing stricter watch rotations, restricting movements at night, and changing ballast practices to reduce vulnerability. Such adjustments raise operating costs and often reduce capacity utilization.

Geopolitical Stakes and Strategic Actors

The Strait of Hormuz is more than geography: it is a stage for geopolitical signaling. Regional states with interests include the Gulf monarchies that export hydrocarbons, Iran whose coastline flanks the strait, and nearby states whose ports and facilities can act as intermediate hubs. Extra-regional powers—navies and air forces from distant capitals—also play a role because they have strategic and commercial stakes in keeping trade flowing. A blockade can be deliberate state strategy, a non-state interdiction, or an unintended consequence of conflict; each scenario requires a different diplomatic and military response.

US Navy Gulf escort

Winners, Losers, and the Distribution of Costs

No disruption is evenly felt. Energy exporters who can redirect flows to alternative terminals and pipelines may mitigate revenue losses, while import-dependent countries—especially those in Asia without diversified suppliers—suffer earlier and harder. Insurance and freight costs are shared across shippers and consignees, but small and medium-sized firms usually have less leverage to renegotiate shipping terms or absorb surcharges. Refineries with flexible crude slates can adapt, while those configured for specific grades may face operational challenges or shutdowns.

Short-, Medium-, and Long-Term Scenarios

Scenarios matter. In a short-term disruption (days to a few weeks) markets may experience price spikes and temporary rerouting; inventories and strategic reserves usually suffice to prevent famine-level shortages. In a medium-term disruption (weeks to months), shipping capacity tightens, insurance premiums remain elevated, and manufacturing schedules slip. Long-term or repeated disruptions (months to years) would reshape trade flows: new pipelines, expanded port capacity, or supranational policy shifts could be pursued to reduce vulnerability—but such projects take time and capital and rarely deliver immediate relief.

Economic and Financial Channel Impacts

Financial markets price risk quickly. Currency volatility can hit petro-dependent economies, while equity markets revalue energy companies and global shipping firms differently depending on exposure. Credit spreads for companies with heavy trade finance needs may widen, reflecting repayment risk when cargo is delayed or diverted. Central banks and finance ministries may need to coordinate on measures ranging from targeted subsidies to using sovereign strategic reserves to calm domestic markets.

Ports and Regional Logistics: Where Congestion Forms

Rerouting concentrates traffic at alternative choke points. Ports in the Arabian Sea, East Africa, and South Asia could see sudden spikes in calls. If port handling capacity, hinterland connections, or berth availability are insufficient, ships idle at anchorage and container dwell times grow. That increases demurrage and detention charges, complicates container re-positioning, and squeezes global slot availability. Logistics providers may prioritize high-margin goods, leaving lower-margin but essential cargo to wait.

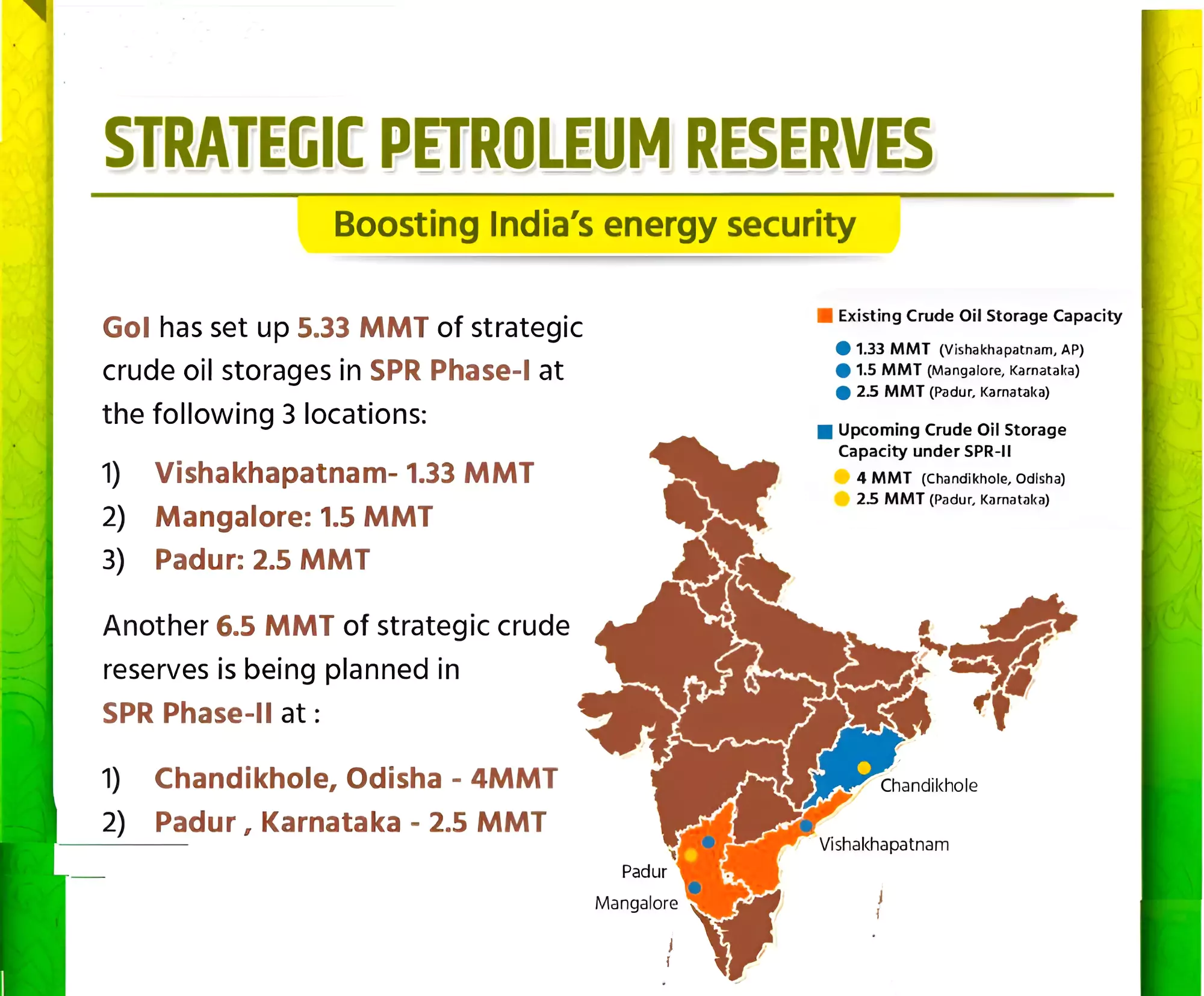

Energy Security: Stocks, Substitutes, and Policy Responses

Countries worried about energy security have a toolkit: release strategic petroleum reserves, impose temporary fuel allocations, incentivize substitution (e.g., switching fuel types or increasing efficiency), and increase domestic production where feasible. These measures are politically charged—releasing reserves affects market psychology and domestic politics, while subsidizing fuel can strain public finances. The strategic calculus weighs immediate relief against long-term price signals that influence investment in alternatives and capacity.

Strategic petroleum reserves storage

Private-Sector Responses and Contingency Planning

Companies should treat a Hormuz blockade as both a geopolitical event and a complex logistics problem. Practical steps include stress-testing supply chains against longer transit times, increasing buffer inventory for critical components, diversifying suppliers geographically, and ensuring contracts contain flexible force majeure language. Corporations that proactively secure alternative shipping arrangements or buy contingent insurance can reduce operational surprises—and sometimes gain bargaining advantage when capacity is tight.

Legal, Insurance, and Contractual Considerations

Maritime contract law and insurance clauses become highly relevant. Force majeure declarations, demurrage claims, and charterparty disputes often follow disruptive events. Legal teams should review contract language to understand liabilities and potential remedies. Likewise, companies buying war-risk insurance must assess coverage windows and exclusions; not all policies behave the same under political or military incidents.

Longer-Term Strategic Adjustments

Persistent or repeated disruptions can catalyze infrastructure changes: new pipelines, LNG terminals in consumer markets, and expanded transshipment hubs further from the Persian Gulf. Diversification into renewables and a strategic shift in energy consumption patterns would slowly reduce the global economy’s vulnerability to maritime chokepoints. But these transitions require coordinated public policy, private investment, and time—often measured in years, not months.

What Governments Can Do

Policy responses include immediate diplomatic engagement, naval presence to protect commercial traffic, and multilateral coordination to keep insurance and trade finance flowing. Longer-term policy might focus on stockpile strategies, incentives for alternative routes or fuels, and investment in port and hinterland resilience. Importantly, transparent communication by authorities reduces market panic and helps businesses plan more effectively.

How Businesses Should Prepare — A Checklist

Practical recommendations for companies with exposure to the region:

- Map exposure: quantify the share of supply and revenue tied to transits through Hormuz.

- Stress-test: run scenarios for 1, 4, and 12-week disruptions, measuring financial and operational impacts.

- Diversify: identify alternative suppliers, ports, and carriers outside the chokepoint.

- Inventory strategy: increase critical inventory selectively; avoid blanket stockpiling that strains cash flow.

- Insurance review: confirm war-risk and contingency coverage and exclusions.

- Contract review: update force majeure clauses and shipping terms to reflect geopolitical risk.

Case Study Snapshot: Historical Lessons

Past incidents—temporary closures, attacks on tankers, or heightened tensions—offer instructive lessons. Markets often overreact in the first days, then recalibrate as physical flows find workarounds. Businesses that reacted by diversifying suppliers or increasing buffer stocks fared better than those that waited for conditions to normalize. Most importantly, repeated small disruptions change behavior: buyers build resilience where before they accepted efficiency as the sole priority.

Conclusion: Strategic Resilience over Short-Term Reaction

A blockage of the Strait of Hormuz would be a test of global economic resilience. The short-term consequences—price spikes, rerouting, and insurance shocks—are painful but manageable for many economies. The medium-term effects expose structural vulnerabilities in logistics, port capacity, and energy dependence. The right response blends immediate action (diplomacy, reserve releases, operational mitigation) with longer-term strategic investments (diversification of supply, port and pipeline capacity, energy transition). For businesses and governments alike, the lesson is clear: resilience pays. Preparedness reduces panic, preserves market functioning, and limits the socioeconomic cost of a crisis that, by geography, is deceptively small but globally consequential.

- Hormuz is a small physical bottleneck with global economic reach.

- Immediate impacts are felt most acutely in energy markets and shipping costs.

- Rerouting is possible but expensive and creates new bottlenecks.

- Insurance and contract clauses materially affect who bears costs.

- Long-term resilience requires infrastructure investment and diversified sourcing.

This article explains likely impacts and practical responses; it does not predict any single political outcome.