Shorting a Country: How Investors Bet Against an Economy

It sounds extreme: how do you short an entire country? The phrase captures a real activity in global finance — investors and funds taking positions that profit when a nation's economy, currency, or creditworthiness weakens. This article breaks that idea down into practical instruments, the macroeconomic signals traders monitor, legal and ethical boundaries, and how a careful planner would construct and manage such a strategy. Whether you are an advanced individual investor, a portfolio manager, or simply intellectually curious, the goal here is to translate headline-grabbing bets into clear mechanics and disciplined risk control.

Understanding the Concept

What does it mean to "short" a country?

Shorting a country is shorthand for positioning to profit from an adverse move in a country's economic profile. That profile includes its currency value, sovereign bond prices, equity markets, commodity revenues (if the country is a major producer), and the perceived risk of default or restructuring. An investor can target one or more of these exposures — each offers different potential returns, time horizons, and styles of risk.

Why investors make these trades

Investors short a country for several reasons: to hedge exposure in an international portfolio, to speculate on macroeconomic deterioration or political instability, to arbitrage mispriced credit relative to fundamentals, or to express a bearish macro view as part of a diversified macro strategy. Sometimes the motive is defensive: corporations and funds use these positions to protect gains elsewhere.

Shorting a country is less a single bet and more a basket of targeted exposures — currency, credit, equities, and commodities — each with its own mechanics.

Mechanisms to 'Short' a Country

Currency: direct FX shorts and forwards

One of the most direct ways to bet against a country is to short its currency. Traders can sell the local currency against a stronger currency using spot FX, forwards, or non-deliverable forwards in restricted markets. Currency positions can be highly liquid and react quickly to new information — central bank comments, inflation surprises, or political shocks. But currencies often move violently and can be affected by central-bank intervention, capital controls, and funding costs.

currency short trading

currency forward contract

Sovereign bonds and yields

Sovereign bonds are essentially loans to a country. Shorting bonds can be achieved by selling long-dated government bonds, using futures contracts where available, or by buying protection via credit default swaps (CDS). When bond prices fall, yields rise. A rise in yields indicates increased credit stress. Shorting bonds is attractive when the market underestimates fiscal stress, rising deficits, or the probability of restructuring.

sovereign bond shorting

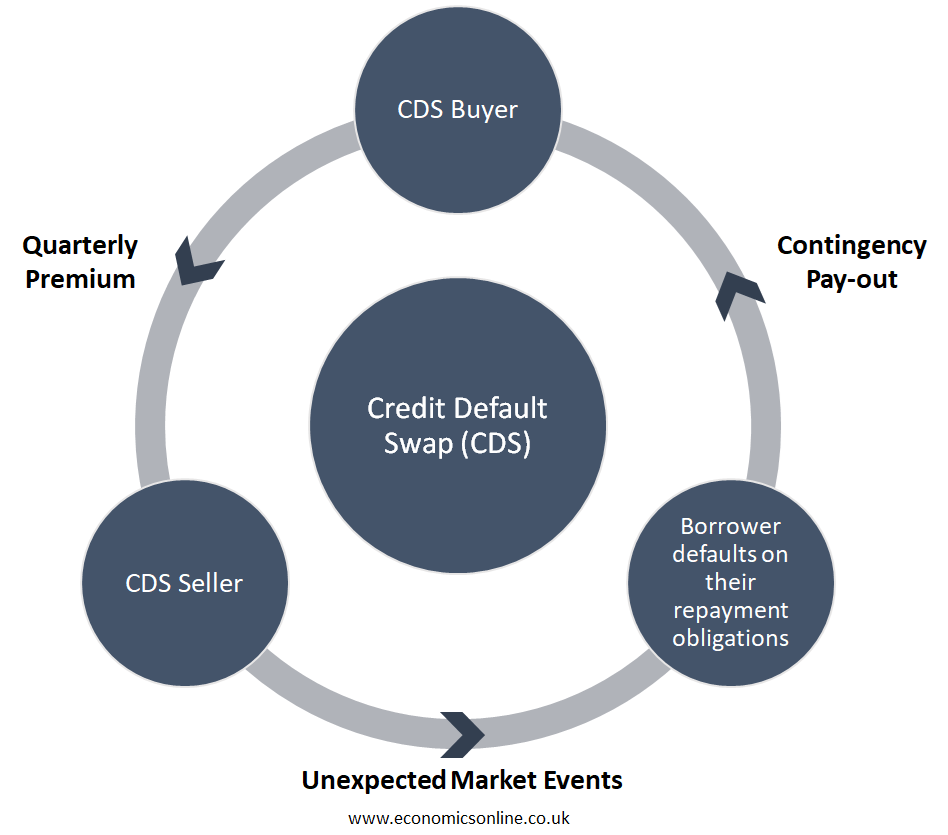

Credit Default Swaps (CDS)

CDS are the primary instruments investors use to take directional credit risk on sovereign issuers without owning the bonds. Buying CDS protection pays off if the sovereign restructures or defaults, or if credit spreads widen significantly. CDS markets can be less liquid for smaller or emerging sovereigns and may carry counterparty and basis risk.

credit default swap CDS

Equities: short selling and synthetic exposure

Shorting equity markets of a country — either individual stocks or indices — is a way to express a view on growth and corporate profitability in that jurisdiction. Short exposure can be obtained through margin shorting, buying put options, or using inverse ETFs where available. For thin markets or where direct shorts are restricted, investors can use international ADRs or derivatives on broad indices to create a synthetic short.

ETFs and pooled vehicles

Exchange-traded funds make it easier for many investors to take a macro view. Inverse or leveraged ETFs that target country indices or currencies allow a packaged short exposure. However, these are typically designed for short-term tactical bets and suffer from path dependency and daily resetting that can erode returns over longer horizons.

Commodity channels and trade exposures

For commodity-exporting countries, a decline in commodity prices can cripple public finances and currency value. Investors can short commodity-linked equities or use futures to bet on falling commodity prices — an indirect but powerful way to short a commodity-dependent economy.

Designing a Strategy

Research and signal generation

Successful macro positions start with a framework for signals. Those signals can include persistent trade deficits, rising inflation, a deteriorating fiscal balance, falling foreign-exchange reserves, widening current-account deficits, political instability, or a loss of confidence by foreign investors. Quantitative overlays can automate detection: yield spread widening, CDS spread jumps, or currency declines beyond technical support levels are typical triggers.

Position construction

Construct the position with clarity: what exactly are you shorting, what is your time horizon, and what are your performance objectives? Use instruments that match the horizon — futures and options for near-term tactical bets, CDS and long-dated bond positions for structural views. Consider pairing exposures: shorting a currency while buying CDS can create a more balanced trade if currency weakness is accompanied by credit stress.

macro hedge fund strategy

Sizing and leverage

Size matters. Overleveraging is the most common pitfall when betting on macro moves. Use position-sizing rules tied to volatility and tail-risk budgets. For example, allocate to a trade no more than a predetermined percent of capital and define maximum acceptable drawdown. Remember funding costs: currency shorts can carry swap costs; bond shorts may require borrowing bonds; CDS premiums are paid periodically.

Risk management and exit rules

Define stop-loss levels, scenarios that invalidate your thesis, and explicit exit rules. Market liquidity can vanish during stress, leaving positions difficult to unwind. Maintain contingency plans such as hedging collars, option-based loss caps, or staggered position exits. Daily monitoring of macro indicators and market microstructure is essential.

Legal, Operational, and Ethical Considerations

Legal and regulatory constraints

Not every instrument is available in every market. Some countries impose capital controls that prevent or tax currency shorts, restrict derivative warranties, or limit short selling of domestic equities. Funds and individuals must comply with local regulations, tax regimes, and reporting requirements. Operationally, borrowing assets for shorts may be limited or expensive.

Ethical implications

Shorting a country raises ethical questions. Aggressive positioning can amplify market stress and may be seen as profiting from a population's hardship. Some investors reconcile this by focusing on hedging existing exposures, engaging in constructive dialogue with sovereign debtors when active in restructurings, or avoiding trades that may flare humanitarian crises. Ethics intersect with reputation risk — large public bets invite scrutiny.

Practical Step-by-Step Example

Scenario: an emerging market with rising deficits

Imagine a country with widening fiscal deficits, dwindling FX reserves, and accelerating inflation. A logical, measured approach to shorting would be:

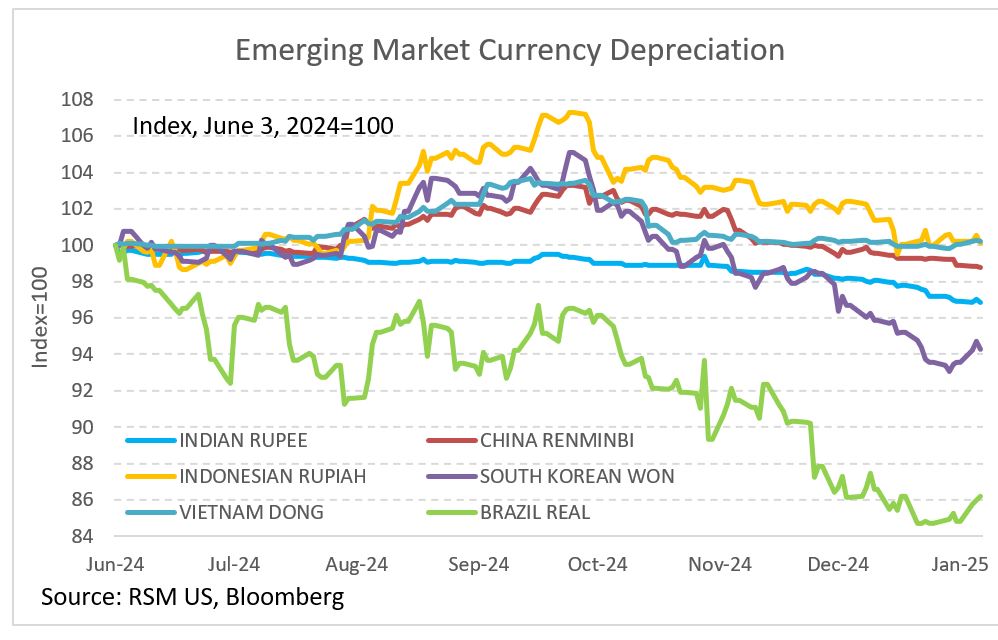

emerging market currency devaluation

- Research — Verify fiscal accounts, reserves, and maturity wall of sovereign bonds; monitor central bank foreign-exchange intervention history.

- Define horizon — Choose a 6–24 month horizon for a structural trade given the fiscal timeline.

- Select instruments — Buy sovereign CDS to express credit risk; short the currency via forward contracts; selectively short export-exposed equities or buy put options on an index.

- Size conservatively — Limit the combined exposure to a fraction of total portfolio capital and allow for margin and roll costs.

- Hedge tail risk — Use options to cap losses or maintain a cash buffer.

fiscal deficit country

Throughout, maintain watchlists for indicators that would invalidate the thesis: surprise reserve replenishment, a credible austerity program, or swift central-bank rate hikes that restore confidence.

Common Pitfalls and How to Avoid Them

Timing risk

Macro trades can be right for the wrong reason or right but too early. A country can sustain unsustainable policies for years before a market re-prices. To manage timing risk: scale positions, use options for defined risk, and avoid one-way leverage that forces liquidation on temporary pain.

Funding and basis risk

Costs to maintain a short position can eat returns. Currency carry costs, CDS premium payments, and borrowing fees on bonds or equities are real expenses. Additionally, basis risk — the gap between CDS moves and bond price moves, or between currency moves and equity moves — can create confusing P&L paths and needs active management.

leverage and margin risks

Liquidity and market closures

In times of stress, markets may close, spreads widen, and short squeezes can explode. Maintain a liquidity contingency and avoid concentrated positions in illiquid instruments unless you have a clear exit plan with counterparties.

Case Studies — Patterns, Not Prescriptions

Sovereign credit crises

History shows common patterns: a shock (commodity collapse, political change, or global tightening) pressures a balance sheet; reserves fall and yields spike; capital controls or restructurings follow. Investors who identified the balance-sheet stress early and used protective instruments often fared better than those who tried to pick the exact moment of default. But remember: every country has unique institutional and political dynamics.

Market-driven currency collapses

Currency moves can be swift and devastating. Some attacks succeed because local banks or investors are overweight domestic assets, creating crowded long positions that unwind quickly. Others fail because central banks defend the peg or impose capital controls. Effective strategies anticipate both outcomes and size exposures accordingly.

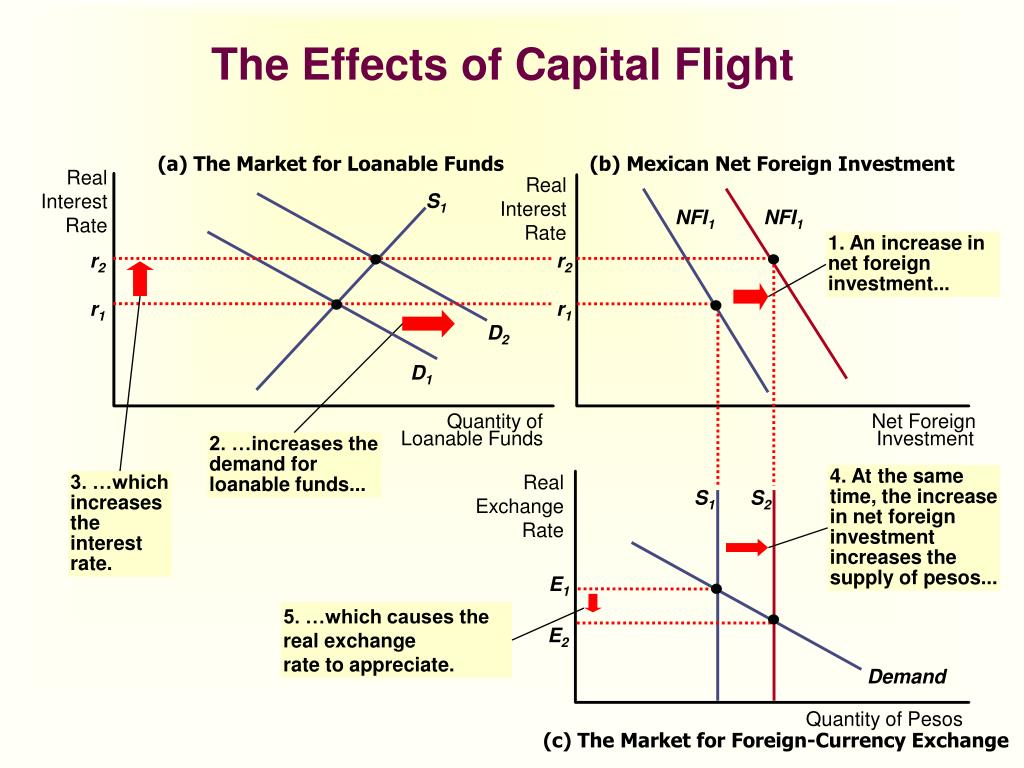

capital flight market stress

- Powerful hedge against concentrated emerging-market exposure.

- Potential outsized returns if the market misprices sovereign risk.

- High funding, liquidity, and timing risk.

- Legal and reputational pitfalls.

Ethical Checklist and Responsible Practices

Questions to ask before placing a trade

- Is this a hedge or a speculative bet? Prioritize hedging legitimate exposures over public speculation for reputational safety.

- Could this trade exacerbate harm? Avoid trades that deliberately induce market panic or exploit fragile humanitarian situations.

- Are you complying with regulations? Confirm local and international regulatory constraints and reporting obligations.

ethical investing sovereign risk

Conclusion

Shorting a country is less an act of aggression and more a set of financial techniques that target distinct economic exposures. From currency and sovereign credit to equities and commodities, there are multiple levers to express a bearish view. The discipline lies in rigorous research, matched instrument choice, careful sizing, and robust risk controls. Equally important are legal and ethical safeguards that protect both capital and reputation.

- Shorting a country involves targeting currency, credit, equity, or commodity exposures, not a single 'country short'.

- Use instruments that match your horizon: FX and options for tactical plays, CDS and bond positions for structural views.

- Manage timing, funding, and liquidity risk with conservative sizing and explicit exit rules.

- Consider legal constraints and reputational impacts before publicizing macro bets.

If you're contemplating such strategies, start small, document a clear thesis, and treat these trades as part of a broader portfolio plan rather than as isolated, headline-seeking gambits. With disciplined execution they can be an effective tool — without discipline they can become a costly lesson in the power of macro volatility.