Oil Prices Fall After US–Iran Deal: Market Impact and Outlook

The immediate reaction was unmistakable: benchmark crude futures dipped as trading desks recalibrated a political story into a supply story. What began as diplomatic headlines about an agreement between Washington and Tehran quickly translated into chart moves, position squaring, and a broader reassessment of how much crude could flow back into world markets over the coming months. For traders, refiners, and policymakers this is more than a price swing — it is a test of assumptions about risk, capacity and the speed of reintegration.

What Happened — The Headlines and the Market

The announcement of a US–Iran deal removed some immediate tail risk associated with a prolonged confrontation between the two governments. Markets reacted by shedding part of the so-called geopolitical risk premium that had been embedded in crude prices. The result: measured declines in Brent and West Texas Intermediate (WTI) contracts, increased volatility in short-dated futures and options, and a flurry of repositioning by speculators and hedgers.

That market move reflects a simple logic: if sanctions are relaxed and Iranian barrels can reach international buyers more easily, global supply effectively expands. Even if actual incremental flows take months to materialize, futures prices often front-run physical changes because traders price in expectations. For companies and consumers, the consequences are multi-layered — lower fuel costs at the pump, altered margins for refiners, and renewed competition for market share among exporters.

US Iran diplomatic agreement

Why Prices Slid: Economics of a Diplomatic Shift

To understand the price response, it helps to unpack three dynamics that move commodities quickly: supply expectations, risk premia and liquidity flows. The US–Iran deal affected all three.

First, the supply expectation changed. Markets began to anticipate that Iranian exports could, over time, increase from current constrained levels toward pre-sanctions production capabilities. That possibility reduces the marginal scarcity the market had been pricing.

Second, the geopolitical risk premium contracted. For months, elevated geopolitical tensions between Iran and the US had supported a premium — a buffer in prices that compensates for the risk of sudden disruptions. When that buffer looks less likely to be triggered, market participants are willing to accept lower prices.

Third, liquidity and positioning adjusted. Short-covering, profit-taking on long positions and a rotation into other assets — bonds, equities or currencies — all add to downward pressure in the immediate hours and days after the news. Volatility often spikes in such transitions as models and human traders re-run their scenarios.

A diplomatic breakthrough can be as powerful as a production increase in changing market psychology.

How Much Iranian Supply Could Return — Near Term vs Longer Term

One of the central questions is timing. Markets instinctively ask: how many barrels, and when? The answers are layered and hinge on operational and political factors.

Near-term constraints matter. Even if sanctions are loosened, physical export capability depends on fields, pipelines, shipping capacity and buyers willing to transact. Iran’s upstream infrastructure has been affected by years of underinvestment and sanctions-era maintenance backlogs; ramping production requires time, capital, and often foreign technology.

Over the medium term, however, the potential is significant. Iran has large undeveloped reservoirs and historically exported millions of barrels per day before restrictions. If investment flows resume and foreign partners return, production could rise substantially over one to three years. Markets will price a probabilistic path between the conservative short-term reality and the more expansionary long-term potential.

OPEC+ meeting conference room

Market Participants: Winners, Losers and Those in the Middle

Different actors experience the shock differently.

- Refiners and consumers: Lower crude feedstock costs help refining margins and, ultimately, retail fuel prices. For countries that import petroleum products rather than crude, the effect is indirect but still positive through lower crude-driven input costs.

- Oil producers (non-Iran): Exporters with slim margins or high fiscal breakevens feel pressure. Countries that rely heavily on oil revenues for budgets face policy choices: cut output, accept lower prices, or seek fiscal adjustments.

- OPEC+: The producer group may reassess production targets. Any significant return of Iranian barrels complicates the delicate balance OPEC+ has managed between supporting prices and defending market share.

- Investors and speculators: Hedge funds and commodity desks that were net long may book losses or reduce exposure, while shorts profit. Long-only investors reassess forward curves and reprice energy allocations.

OPEC+ and the Politics of Market Share

For OPEC+ members, a return of Iranian supply is a thorny political and economic problem. On one hand, the group prefers higher prices to meet fiscal needs of member states. On the other, ignoring additional global supply can cede market share to Iran. The group’s customary response has included coordinated production cuts or phased output adjustments. However, coordination becomes more difficult when members have diverging fiscal pressures and geopolitical priorities.

Expect negotiations, behind-the-scenes diplomacy, and potentially a recalibration of quotas. The real question is whether OPEC+ can deliver credible countermeasures quickly enough to alter market expectations, or whether the market will internalize the new supply prospects and drive prices lower for an extended period.

Economic Implications Beyond the Pump

Lower oil prices have broad macroeconomic implications. For consuming economies, cheaper energy lightens inflationary pressure, can support consumer spending and improve real incomes. For producers reliant on oil revenues, lower prices mean tighter budgets and possible spending cuts, with knock-on effects on growth.

For central banks, lower energy-driven inflation can change policy conversations. If oil eases substantially, it may reduce the urgency for aggressive rate hikes in regions where energy is a major inflation component. Conversely, countries dependent on oil exports might face fiscal strains that pressure exchange rates and financial stability.

oil tanker shipping Persian Gulf

Trading and Investment Strategies in a Changing Market

Market participants will consider several strategic responses.

Active traders often shift into curve trades: exploiting differences between prompt and later-dated futures contracts. If the market believes Iranian barrels arrive slowly, the forward curve might reflect a steepening or flattening that creates trade opportunities.

Hedgers — airlines, shipping firms, refiners — may seize the chance to lock in lower prices through swaps and futures. Longer-term investors will revisit portfolio weights for energy equities, considering revised cash-flow scenarios for drillers and national oil companies.

Risks and Upside — Why Prices Could Rebound

The initial decline should not be read as permanent. Several risks can push prices back up.

- Non-compliance or delays: If the deal falters, or if political actors (domestic or international) obstruct implementation, the anticipated barrels may not materialize.

- Supply disruptions elsewhere: Unrelated outages in other producing regions, extreme weather, or accidents can tighten the market independently of Iranian flows.

- Strategic responses: OPEC+ could coordinate cuts that offset new Iranian supply, supporting prices at higher levels.

- Geopolitical flare-ups: Even with a deal, regional tensions can persist and reintroduce a premium.

These upside risks mean traders should avoid blanket assumptions. Volatility may remain elevated as the market processes incoming data on shipping, exports, and domestic policy changes in Iran and other key producers.

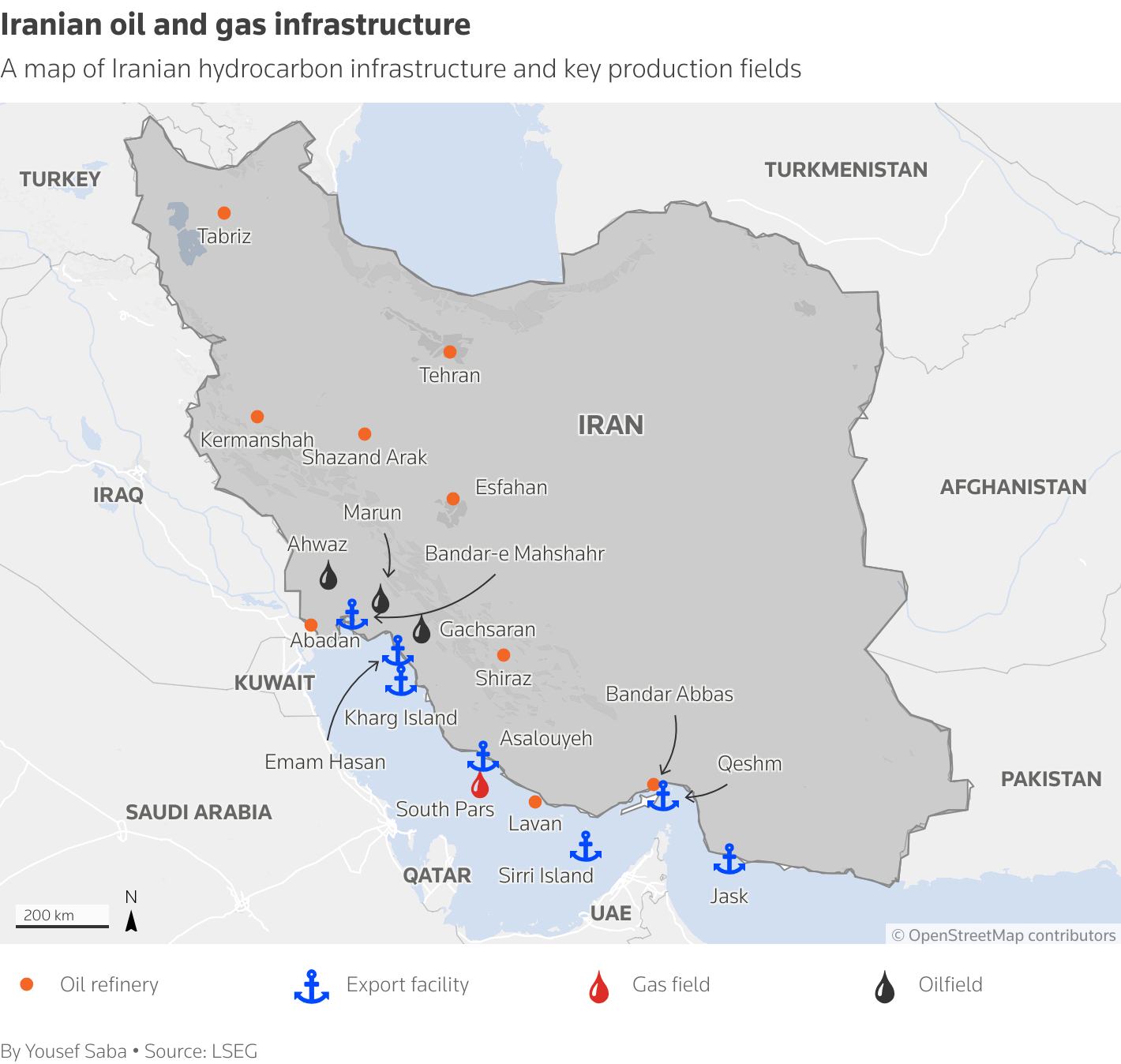

Iranian oil production fields

Regional and Global Winners and Losers

At a regional level, countries importing Iranian oil or those geographically close to its markets may benefit from lower costs and improved supply diversity. Conversely, members of the Gulf Council and other oil-dependent states may face pressure to adjust fiscal balances.

Global manufacturing and transport sectors typically welcome lower energy costs, which can act like a tax cut by reducing operating expenses. For emerging markets that are net importers of fuel, improved terms of trade can bolster growth and help stabilize currencies.

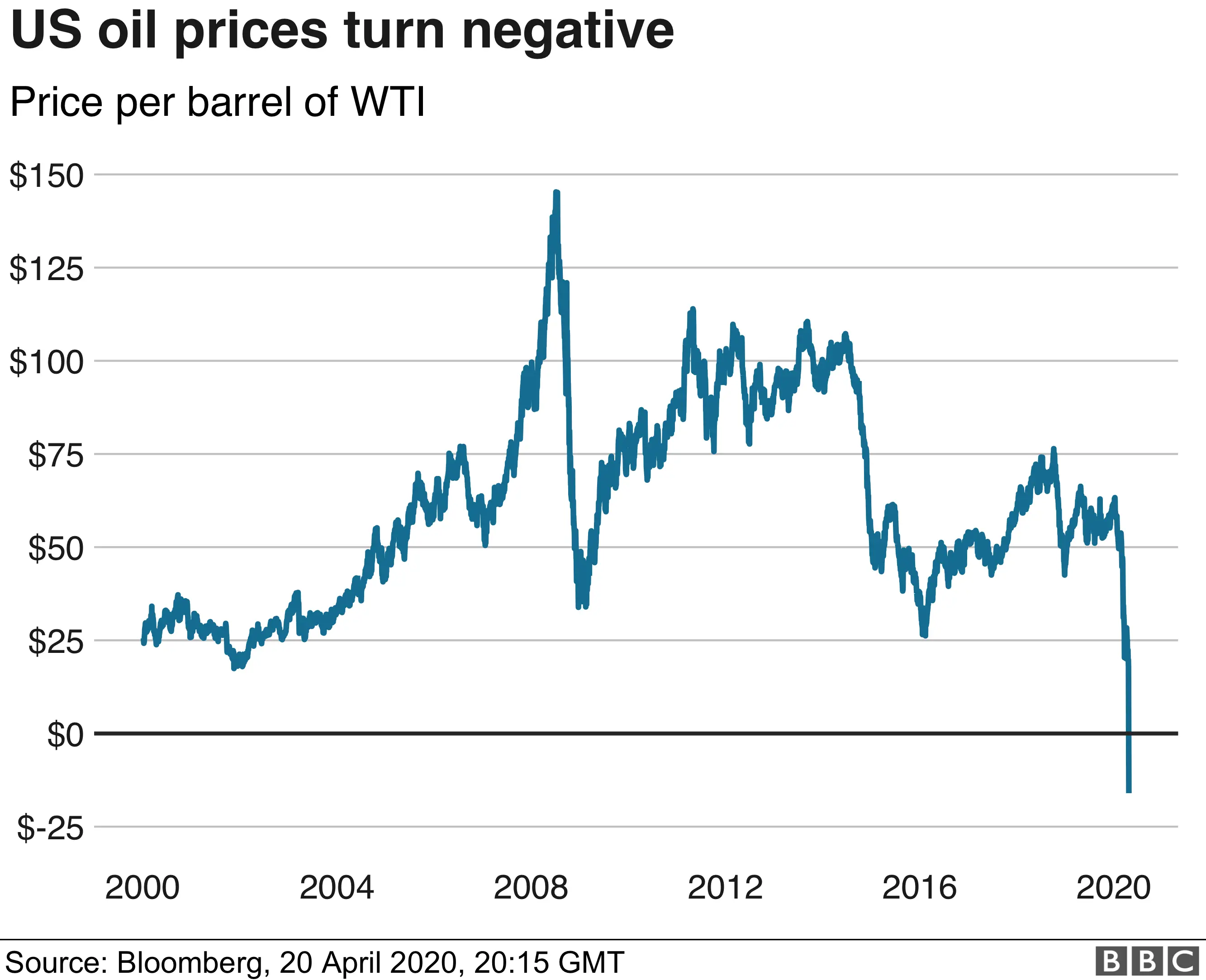

Brent WTI crude oil futures

What to Watch Next — Data and Signals

Markets will now turn attention to several tangible indicators that either confirm or reverse the initial price move:

- Tanker and shipping flows: An uptick in tankers heading to major refining hubs signals real export increases.

- Government export statistics: Monthly and weekly export reports will show whether Iranian volumes are rising.

- Inventory reports: Changes in OECD crude and product stocks are immediate indicators of supply/demand balance.

- OPEC+ statements and meetings: Any coordinated policy responses will be scrutinized for credibility.

- Currency and bond markets: Fiscal reactions by oil exporters often show up in government bond yields and local currencies.

Those data points will determine whether the price move is a transient reaction or the start of a new supply regime.

Longer-Term Structural Considerations

Beyond immediate supply effects, the deal also intersects with longer-term structural trends: the energy transition, investment cycles in upstream oil, and the changing geography of demand. Lower near-term prices can slow the pace of new investment in higher-cost production (deepwater, Arctic, shale expansions), while accelerating demand-side efficiency measures in major consuming economies.

Moreover, a re-integrated Iranian oil sector could shift regional investment patterns, inviting technology partnerships and new infrastructure projects. Over time, those dynamics influence global market structure: who invests, where production grows, and how quickly supply can respond to demand shocks.

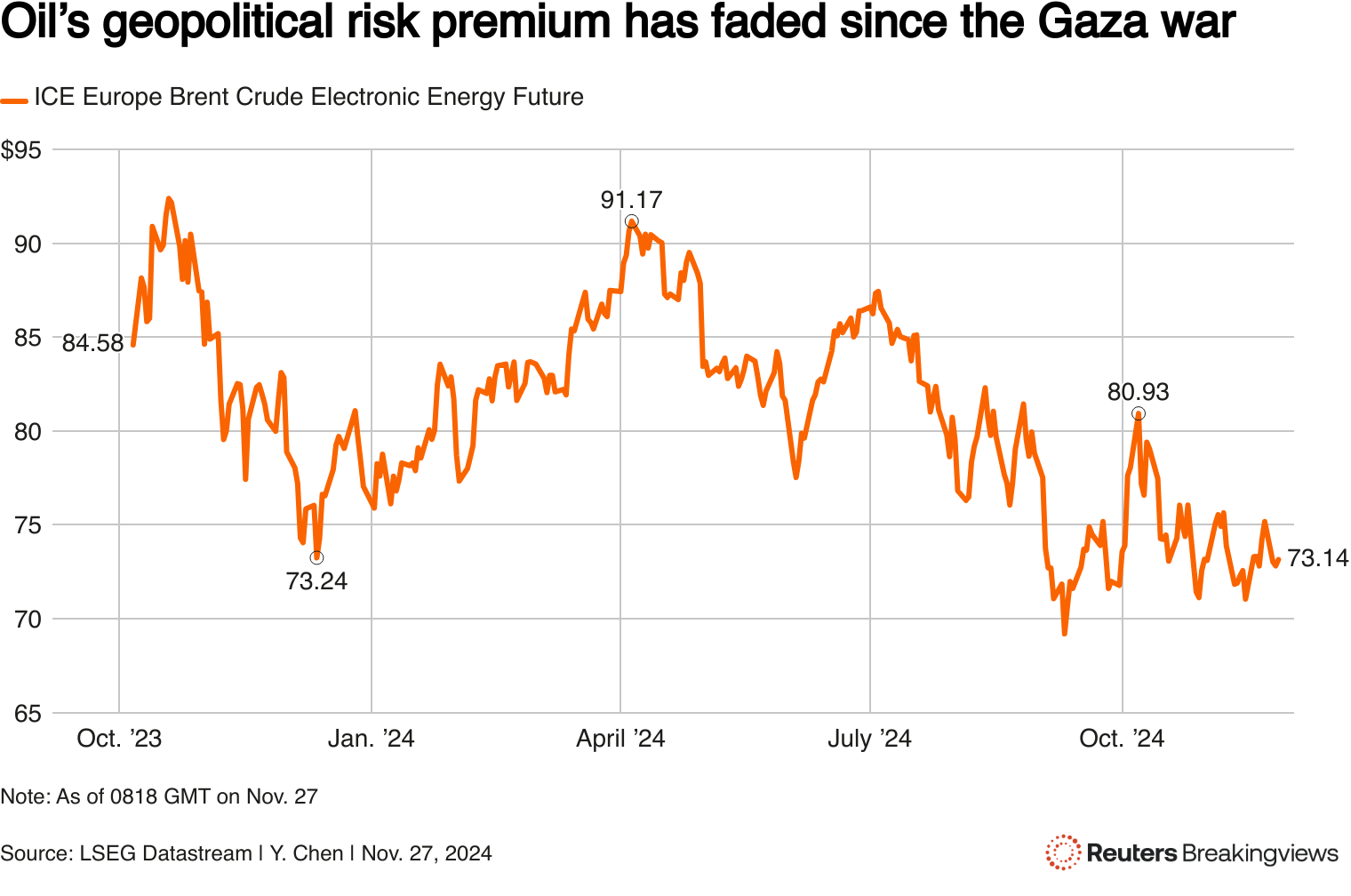

geopolitical risk premium graph

Practical Takeaways for Businesses and Policymakers

For businesses that use oil as an input, the near-term environment offers both relief and a planning challenge. Lower prices reduce immediate cost pressures but increase uncertainty about future price paths. Effective responses include flexible hedging strategies, scenario-based budgeting and attention to operational efficiencies.

Policymakers must balance short-term benefits for consumers with long-term fiscal planning. Oil-dependent states should use windfall revenues prudently when available and build buffers to withstand price swings. Importing countries can view lower prices as an opportunity to accelerate spending on energy efficiency and clean energy investments.

Conclusion — A Market in Transition

The announcement of a US–Iran deal caused oil prices to retrace as markets recalibrated risk and supply expectations. The decline reflects forward-looking pricing that anticipates more barrels reaching global markets, but the path from diplomatic agreement to delivered crude is uncertain and strewn with operational, political and strategic hurdles. Traders will watch physical indicators closely — tanker movements, export statistics, inventory levels and OPEC+ signals — for confirmation.

In the weeks and months ahead, the interplay between expectation and reality will determine whether this price move is a corrective dip or the start of a more durable shift in the global energy equation. For governments, businesses and investors, the prudent response is neither complacency nor panic but disciplined scenario planning, active risk management and close monitoring of the physical market signals that ultimately decide price direction.

- Oil prices fell after a US–Iran agreement, driven by expectations of increased Iranian supply and a reduced geopolitical risk premium.

- Immediate price moves reflect market psychology as much as physical flows; confirmation requires tanker flows and inventory changes.

- OPEC+ coordination, operational constraints, and regional politics will determine the pace at which Iranian barrels return.

- Lower near-term prices help consumers and refiners but add stress to oil-dependent budgets and investment plans.

- Active hedging, scenario planning and watching physical indicators are the best responses for market participants.