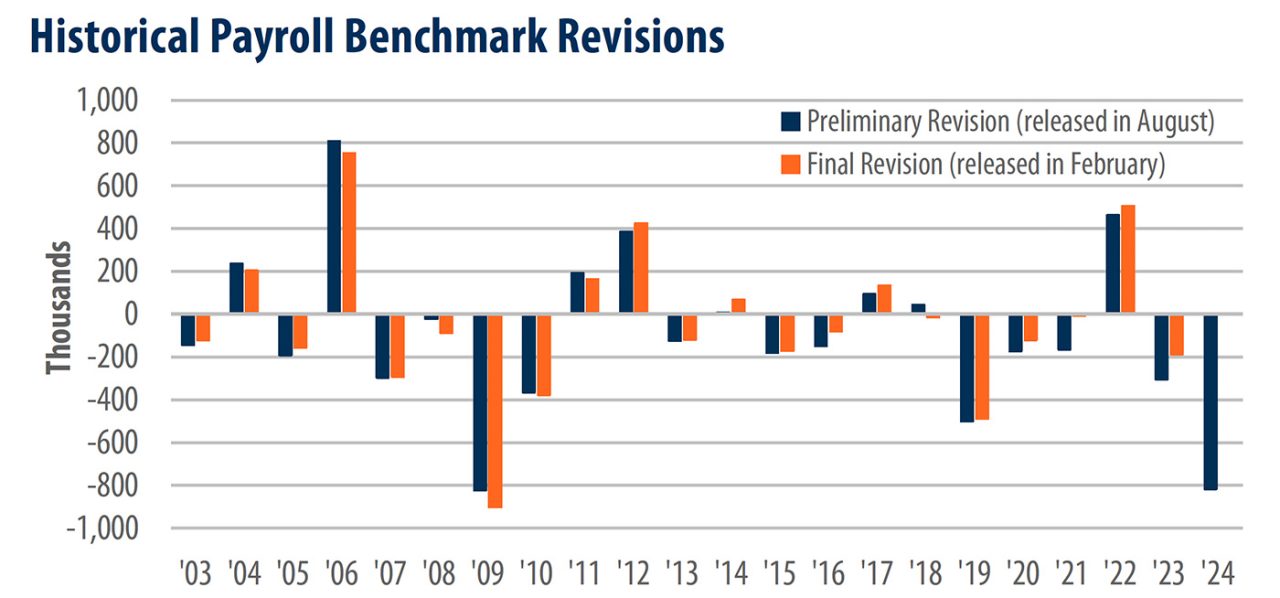

Nearly 1 Million Jobs Lost in 2025 Revision: What It Means

The Bureau of Labor Statistics’ annual revisions to payroll data are routine, but the scale of this year’s adjustment—nearly one million fewer jobs recorded across the 12‑month window surrounding 2025—recasts that year’s labor market from tepid but steady to markedly weaker. For policymakers, business leaders and jobseekers who built plans and expectations around previously published figures, the revision is more than a statistical footnote: it reshapes how we interpret growth, inflation risk, and the capacity of the economy to absorb shocks in the months and years that follow.

Bureau of Labor Statistics revision

A Snapshot: What Changed

The headline: the annual benchmark and related revisions cut previously reported employment gains by roughly nine hundred thousand to just over nine hundred thousand jobs for the measured period, depending on the exact window used. That change lowers average monthly job creation by a material amount, moving America’s labor market out of the ‘robust hiring’ category many observers assumed and into a zone of modest, inconsistent expansion. The unemployment rate, which measures the percent of willing workers who cannot find work, did not spike by the same margin—an important clue that the labor market dynamics behind the revision are subtle and structural rather than purely cyclical.

US payroll data 2025

Why Revisions Happen

Annual and preliminary benchmark revisions are core to how labor statistics remain accurate over time. The BLS issues monthly nonfarm payroll numbers based on a sample survey of businesses, then later reconciles those estimates with administrative data—state unemployment insurance payroll records, tax filings and other complete records—to produce a more definitive count. The difference between early estimates and administrative totals is rarely trivial; it simply became unusually large this time.

labor market statistics

Several factors combine in revisions of this magnitude:

- Administrative updates: Tax and payroll records that arrive late or are reclassified can change industry counts when reconciled with survey estimates.

- Sampling noise: Monthly survey responses are subject to sampling variation; when a year of small monthly swings compounds, the annual correction can be large.

- Classification changes: Reassignments between sectors (for example, from leisure and hospitality to temporary help services or vice versa) shift where jobs are counted.

- Shifts in immigration and demographics: Lower net international migration reduces the number of new workers entering the labor force and the number of jobs needed to employ them.

- Structural economic shifts: Automation, AI deployment and long‑term sectoral reallocation mean that job openings and hires do not track one‑for‑one with economic output.

Which Sectors Were Hit — and Which Held Up

The downward adjustment was broad but concentrated in a few visible industries. Leisure and hospitality—restaurants, hotels and entertainment—saw particularly large downward moves, reflecting a mixture of seasonal reporting adjustments and reclassification of part‑time, gig and temporary roles. Retail and professional and business services also lost ground in the revised counts. By contrast, some sectors that had appeared fragile in headline reports—health care and some segments of construction—saw smaller net adjustments or even modest upward tweaks in particular months.

leisure and hospitality jobs

That pattern matters: leisure and hospitality and retail are both labor‑intensive and highly sensitive to consumer spending patterns. When their job counts are revised down, it suggests either fewer actual jobs were created than survey data implied or that the administrative records captured employment differently than business respondents reported temperamentally during survey months.

retail trade employment

The revision shrinks last year’s headline job gains and forces a reassessment of wage growth, inflation pressure and how aggressively central bankers can act.

What the Revision Means for Policy and Markets

At the most immediate level, a substantially smaller tally of jobs created in 2025 reduces upward pressure on wages and inflation coming from labor market tightness. Central bankers, who treat labor market slack as a key input into monetary policy decisions, will factor the revised pace of hiring into their expectations for future inflation. A weaker underlying job trend can justify a more patient stance on interest‑rate cuts or even argue for holding rates steady longer than previously expected.

Federal Reserve policy

For markets, the revision recalibrates growth expectations. Equities that had priced in strong consumer spending and robust corporate hiring may need to adjust earnings forecasts. Bond markets react to changing inflation expectations and perceived policy action; a downgraded jobs narrative can translate into lower term premiums or different yield curve dynamics depending on how durable the revision looks.

Regional and Household Effects

National aggregates mask large regional variation. States and metropolitan areas with tourism‑heavy economies or high concentrations of retail employment are disproportionately affected when leisure and retail job counts fall. That translates into slower income gains in those communities and can amplify housing market cooling where local employment underperforms.

At the household level, the revision changes the story for people who made life decisions based on perceived labor market strength—those who postponed retirement, changed careers, or took on mortgage debt expecting steady wage growth. Financial plans tied to assumed consistent monthly hiring now require adjustment, and safety nets, retraining programs and local labor assistance become relatively more important in impacted areas.

economic forecasting 2025

Reading Between the Lines: Unemployment vs. Payrolls

One puzzling aspect of large payroll revisions is that the unemployment rate often does not change proportionally. Why? Payroll counts and the unemployment rate measure related but different things. The unemployment rate comes from a household survey that captures who is looking for work and available to work, while payrolls are compiled from business establishment surveys and administrative records. If hiring slows but people also stop looking for work, the unemployment rate can remain steady even as payroll counts fall.

unemployment rate US

That distinction underscores why analysts look at a suite of indicators—participation rate, job openings, average hourly earnings, underemployment and long‑term unemployment—rather than a single number. In some cases, revisions expose a hidden softening that the headline unemployment rate masked.

The Broader Economic Context

The revision arrived amid other economic crosscurrents: still‑elevated interest rates compared with pre‑pandemic norms, evolving trade policy, slower immigration flows in some periods, and rapid adoption of technologies that change the number and type of workers firms need. Taken together, the revised job tally suggests last year’s economy produced less employment per unit of output than previously thought—either because output was lower than estimated, because firms achieved more productivity per worker, or because administrative measures captured employment more conservatively.

For fiscal planners, slow job creation complicates revenue projections. Lower payroll growth translates to less payroll tax base expansion and may alter short‑term fiscal balances at federal and state levels.

What Businesses and Jobseekers Should Do Now

Companies and individuals alike should treat the revision as new, actionable information for planning rather than as a crisis signal. Practical steps include:

- Employers: Revisit hiring plans and headcount budgets for the year with sensitivity analyses that assume slower demand for labor.

- Workers: Update personal financial buffers and consider upskilling in sectors showing steadier demand (health care, some construction trades, select professional services).

- Policymakers: Use the revised base to recheck labor market programs, unemployment insurance forecasts and retraining investments to ensure they align with current employment realities.

professional services jobs

How to Interpret Future Revisions

Large revisions are disconcerting because they alter the past story and therefore change the counterfactual policymakers used. But they are also a sign the statistical system is functioning: it absorbs better data and updates historical estimates accordingly. Expect further tweaks—monthly numbers will continue to be revised—and remember that historical trends are now likely to reflect somewhat slower job creation than earlier published figures suggested.

job growth revision

Analysts will watch subsequent releases for confirmation: sustained weak hiring in the months after the benchmark suggests a genuine slowdown; a robust bounceback suggests the revision mainly reallocated jobs across months and sectors rather than revealing a persistent decline.

Conclusion

The near‑million‑job downward revision for the 2025 period is a wake‑up call, not an apocalypse. It realigns expectations about how tight the labor market is, tempers inflationary fears born from an overheated hiring narrative, and forces a recalibration of policy, business planning and individual decisions. The adjustment highlights an uncomfortable truth: the economy’s headline strength can mask fragility beneath the surface. Observers should take the revised figures seriously, but also weigh them alongside the full suite of labor indicators and local conditions when making strategic choices.

- The 2025 payroll revision cut nearly one million jobs from previously reported totals, reducing average monthly job gains significantly.

- Major downward moves were concentrated in leisure and hospitality, retail, and professional services, with mixed effects across other sectors.

- Revisions are routine statistical corrections that incorporate administrative data; their size can nonetheless change economic narratives and policy choices.

- Policymakers, businesses and individuals should use the revised data to recalibrate expectations while monitoring subsequent releases for confirmation.