Japan Raises Interest Rate to Its Highest Since 1995

In a decision that marks a clear break with more than three decades of extraordinarily accommodative monetary policy, Japan's central bank has raised its policy interest rate to a level not seen since 1995. The move ends an era defined by persistent low or even negative rates and signals a new phase of policy normalization. For households, firms and global investors, the implications go well beyond a headline figure: higher borrowing costs, renewed currency pressure, changed incentives for savers and a new calibration of risk across asset classes. This article explains why the Bank of Japan acted, how the change will transmit through the economy, and what investors and policymakers should watch next.

Bank of Japan headquarters

WHY THIS MATTERS

Japan's long post-bubble history of low interest rates shaped domestic behavior and international finance for decades. Ultra-low rates suppressed borrowing costs, discouraged savings returns, and supported asset prices while policymakers hunted for persistent inflation and steady wage growth. A return to a higher policy rate — the highest since the mid-1990s — is therefore a structural pivot: it alters incentives for consumption versus saving, raises the cost of servicing debt, and changes the valuation of long-duration assets. It also affects currency markets, because a relative shift in rates can trigger rapid capital flows that move the yen and global funding conditions. In short, this is not a marginal adjustment; it is a regime change with ripple effects across Japan and the world.

CONTEXT: HOW WE GOT HERE

A long march out of extremely easy policy

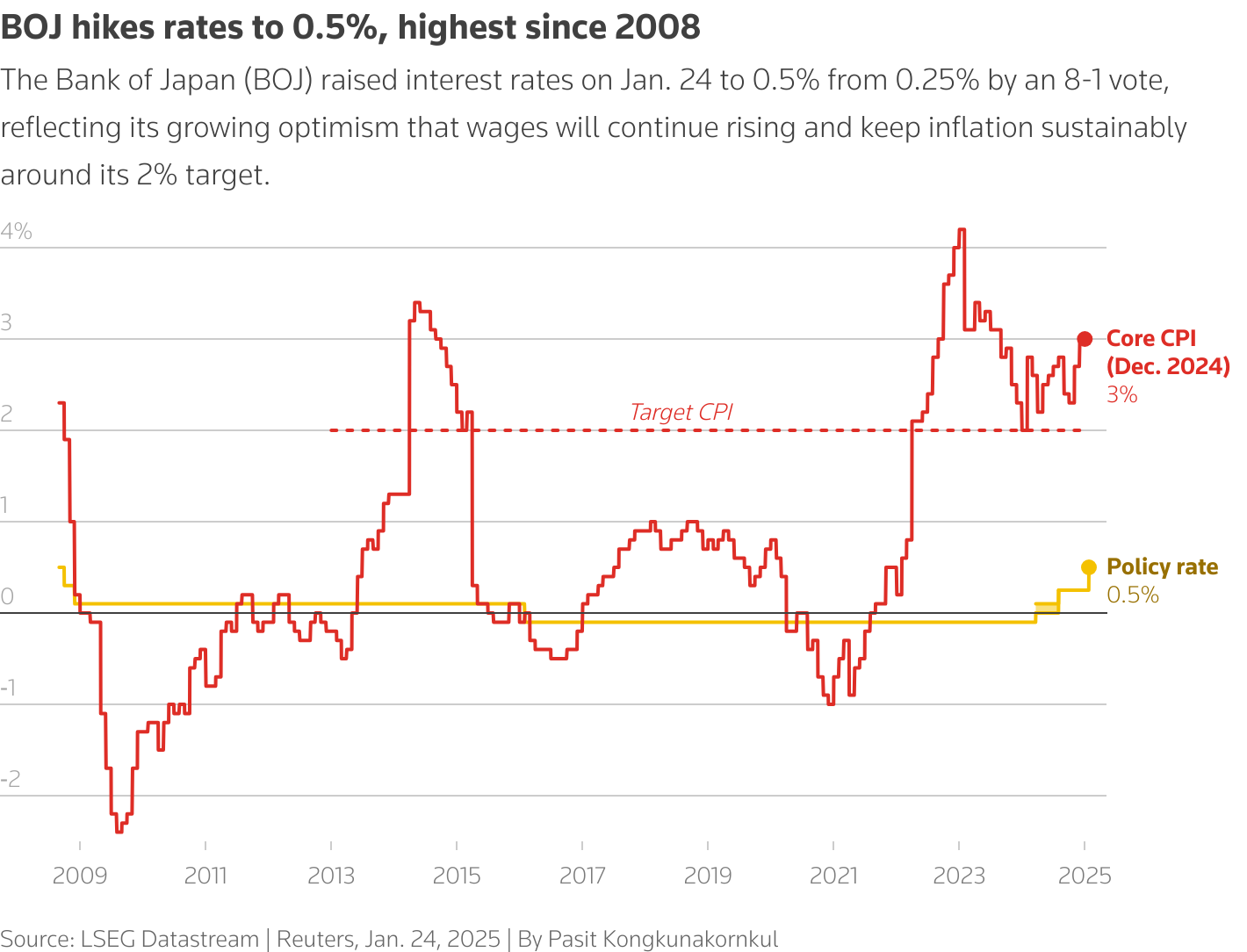

For years the central bank operated with negative or near-zero interest rates and unconventional tools like yield curve control to keep long-term yields pinned near targets. Those policies aimed to spur inflation toward the central bank's target by making borrowing cheap and encouraging risk-taking in asset markets. When inflation pressures began to show more persistence — driven by factors such as higher import costs, stronger wage bargaining in some sectors, and global commodity price shifts — the central bank gradually shifted stance. Small incremental steps became larger moves as price pressures proved more durable than initially expected, and the central bank chose to prioritize price stability over the old paradigm of sustained accommodation.

Global backdrop and policy coordination

The tightening cycle occurs against a backdrop of higher rates around the world. Other major central banks had already been raising rates to tame inflation, prompting capital movement and exchange-rate adjustments. For Japan, which long benefited from cheap funding and the so-called carry trade, higher global rates reduced the appeal of the previous low-rate environment and increased the urgency of restoring domestic policy to a more conventional toolkit. The move must be understood in the context of global monetary convergence: when the policy differentials compress or invert, currencies and asset allocations adjust rapidly.

WHAT THE MOVE MEANS FOR HOUSEHOLDS AND FIRMS

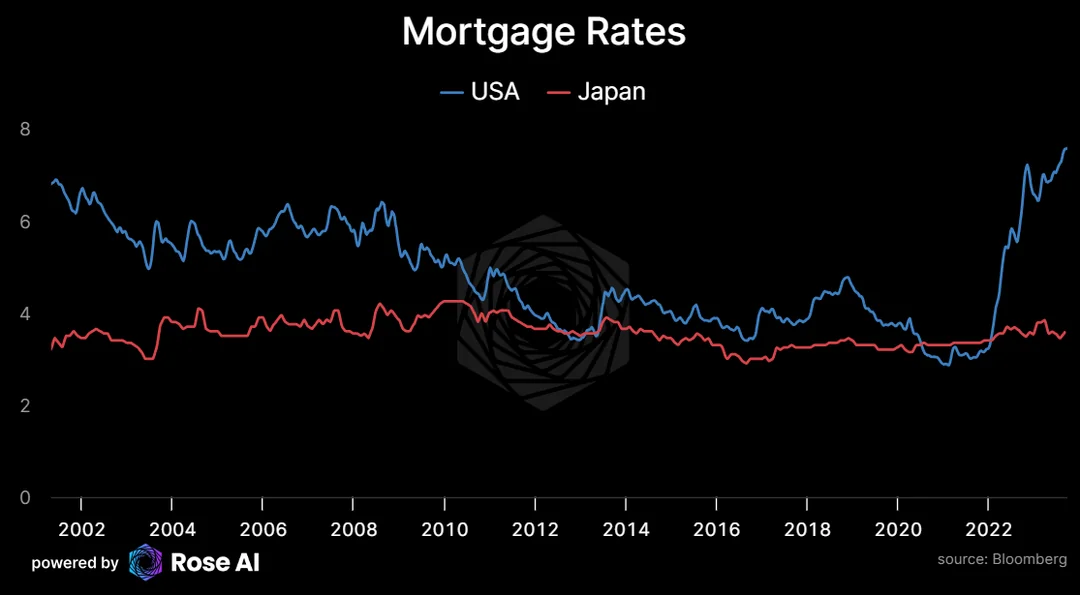

Mortgages, loans and consumer budgets

Higher policy rates eventually filter through to commercial lending and consumer borrowing. For new borrowers the impact is immediate: mortgage offers, personal loans and business credit lines will become more expensive, squeezing disposable income for households and raising financing costs for firms. For variable-rate mortgages or corporate credit with floating spreads, monthly payments will rise, potentially curbing consumer spending and corporate investment. For long-maturity fixed-rate borrowers, the effect will be slower but still material over time as refinancing becomes more costly.

Japanese mortgage rates chart

Corporate balance sheets and investment choices

Japanese firms historically relied on cheap borrowing to fund operations and investment. A higher rate environment forces companies to re-evaluate investment projects — raising the hurdle rate for new capital spending and altering decisions about leverage. Sectors that depend heavily on debt, such as construction and real estate development, will feel the pinch first. Conversely, stronger rates can improve bank margins and profitability, as banks charge more for lending while gradually adjusting deposit offerings.

Corporate borrowing Japan finance

MARKETS AND THE CURRENCY

The yen: from carry trade loser to potential winner

One immediate channel of impact is the foreign exchange market. For decades, Japan's low yields were a backbone for the carry trade: investors borrowed yen cheaply and invested in higher-yielding assets elsewhere. Raising the domestic rate reduces that arbitrage, and can even reverse flows as foreign investors buy yen to capture higher domestic returns. A stronger yen affects exporters negatively by lowering the value of overseas sales when converted back to domestic currency, but it benefits Japanese consumers and importers by reducing the cost of imported goods and raw materials.

Japanese yen currency exchange

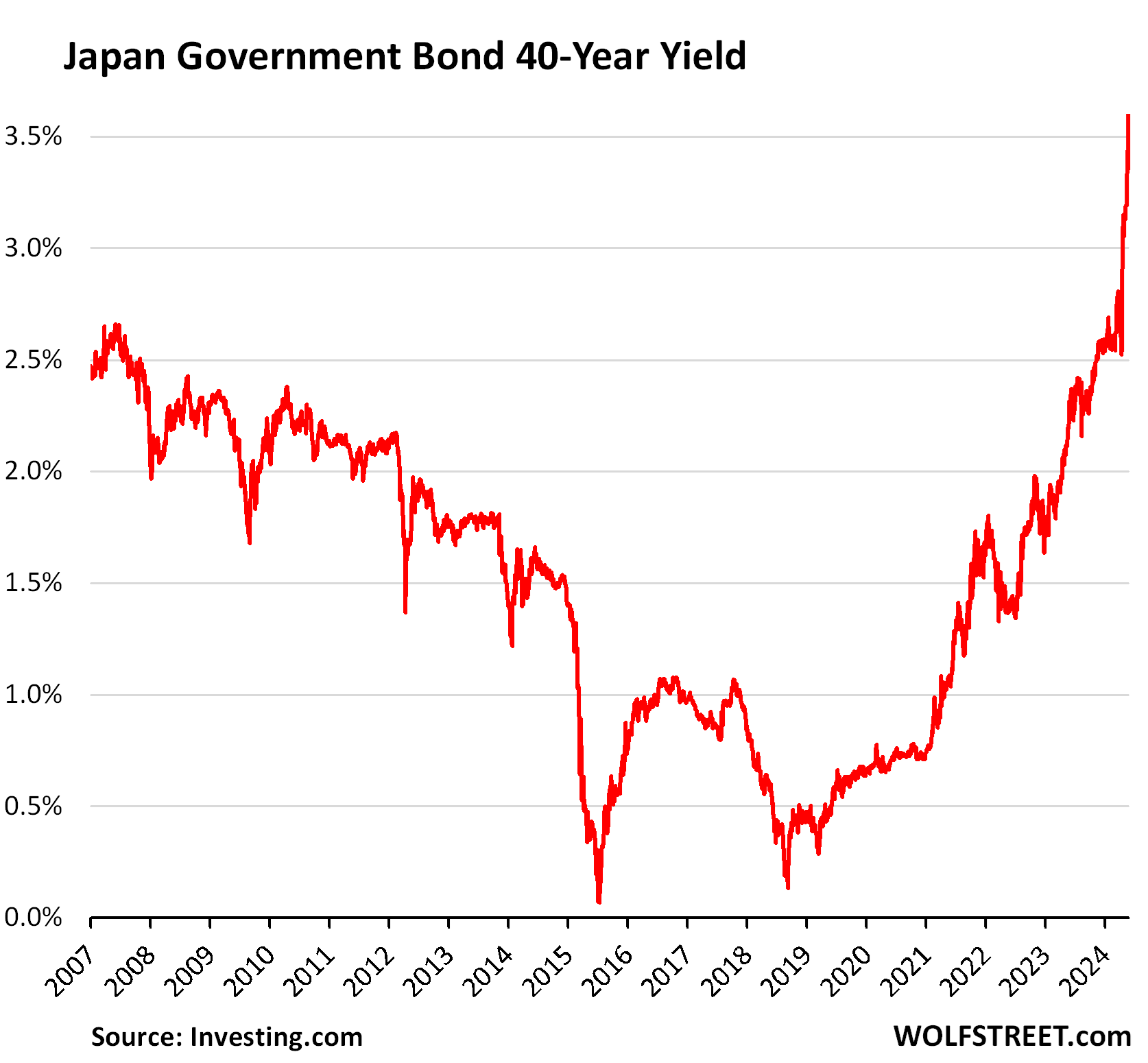

Bonds and the yield curve

Raising the policy rate alters the shape of the government bond yield curve. Short-term yields typically rise first, and the central bank's credibility and communication determine how much long-term yields move. A steepening curve suggests expectations of stronger growth or future inflation. For pension funds and life insurers, a rise in long-term yields can be a blessing: it improves the yields on fixed-income investments that have struggled to meet long-term liabilities. Conversely, if long-term yields spike too quickly, it can create mark-to-market losses on existing bond holdings and disrupt market functioning.

Japan government bond yields

Higher rates mark a regime shift: what was once a world of cheap money now forces every decision — from mortgages to corporate investment — to factor in higher financing costs.

POLICY TRADE-OFFS AND RISKS

Inflation versus growth

The central bank faces the classic tension between taming inflation and supporting economic growth. If rates rise too fast, there is a material risk of tipping the economy into recession: consumer spending can cool, investment can stall, and unemployment may rise. Conversely, if policy is too timid, inflation expectations could become unanchored, eroding purchasing power, real wages and long-term planning. The bank must navigate a narrow corridor where policy slows demand enough to bring inflation back to target without derailing recovery or destabilizing financial markets.

Fiscal implications and government debt

Japan has one of the highest public debt-to-GDP ratios among advanced economies. Higher interest rates increase the cost of servicing that debt, putting pressure on public finances and potentially changing the political calculus around fiscal consolidation and spending priorities. If higher rates persist, the government may face difficult choices between cutting spending, raising revenues, or accepting higher debt burdens — each choice carrying social and political consequences.

WHO GAINS AND WHO LOSES

Winners: savers, certain financial institutions, and fixed income investors

Savers who have long endured near-zero returns may finally see meaningful yields on deposits, benefiting households with conservative portfolios. Banks and insurers can enjoy improved net interest margins over time, and pension funds can more plausibly meet long-term liabilities if long-term yields rise. Fixed-income investors who can tolerate near-term price volatility may benefit from purchasing new issues at higher yields.

Losers: highly leveraged borrowers, exporters and select asset classes

The immediate losers are borrowers with heavy debt loads and sectors sensitive to higher discount rates, such as real estate and certain growth stocks whose valuations rely on low-for-longer discounting. Export-oriented firms may suffer from a stronger yen, and households carrying large mortgages or consumer debt will face budget stress. Investors in long-duration assets may see re-pricing as yields climb.

IMPLICATIONS FOR GLOBAL MARKETS

Japan is a large and open economy whose financial markets are deeply integrated into global capital flows. A significant rate increase reshapes global portfolios: higher Japanese rates reduce the yield advantage of foreign assets, prompting reallocation. Currency moves can affect commodity prices and trade balances in Asia and beyond. Additionally, a change in Japan's monetary stance influences perceptions of global monetary convergence and the prospects for synchronized tightening or stabilization across advanced economies.

Regional spillovers

Asian neighbors that have exposure to trade with Japan, or whose financial systems host significant yen-denominated flows, may feel the impact through tighter funding conditions or currency moves. Emerging markets that borrowed in foreign currencies could experience second-round effects if global risk appetite shifts and funding costs rise broadly.

Asian markets financial district

HOW MARKETS MIGHT RESPOND NEXT

Volatility and calibration

Expect volatility in FX and bond markets in the near term as investors price the new regime and scale positions. Central bank communications will be critical: clear forward guidance about the likely path for policy and contingencies can calm markets. Financial authorities may also use macroprudential tools if higher rates trigger asset price dislocations or rapid credit tightening.

Investment strategies to consider

For cautious investors, the normalization offers opportunities and risks. Shorter-duration fixed-income instruments bought at higher yields can provide improved income with limited price sensitivity. Diversifying currency exposure and reviewing leverage in portfolios is prudent. For equity investors, sector rotation may be advisable: financials may outperform while high-growth, high-duration names could lag until rate stability returns.

POLICY SIGNALS TO WATCH

Forward guidance and balance sheet moves

Observe the tone of central bank communications carefully. The bank's language about future rate paths, inflation tolerance and the use of balance-sheet tools will determine market expectations. If policymakers signal a gradual, data-dependent approach, markets may settle quickly. If they leave the door open to more aggressive tightening, expect pronounced volatility.

Wage growth and inflation data

Key indicators to watch include headline and core inflation measures, wage growth and inflation expectations. Sustainable policy normalization depends on whether wages rise enough to support real incomes as prices adjust. If price growth is driven only by temporary factors, the central bank may need to recalibrate; if wages follow, the new normal may be durable.

SCENARIOS AND FORECASTS

Scenario A: Gradual normalization with soft landing

In this optimistic path, wage gains materialize slowly but sustainably, inflation retreats toward target without a sharp growth slowdown, and financial markets adapt with manageable volatility. Corporate investment adjusts, the fiscal burden stabilizes, and policy is able to take a data-dependent, steady approach.

Scenario B: Policy overshoot leads to slowdown

If rates rise too far or too fast, consumption and investment could weaken materially, raising unemployment and triggering a sharper downturn. In this case, policymakers may pause or reverse course, but the transition would be painful for highly indebted sectors and could leave lasting scars in labor markets.

Scenario C: Sticky inflation and further tightening

If inflation proves more persistent than expected — perhaps due to sustained wage increases or structural shifts in import prices — the central bank may need to tighten further. This scenario raises both the cost of public debt and the probability of financial stress in leveraged sectors.

CONCLUSION: WHAT TO DO NOW

Japan's move to a policy rate not seen since 1995 is a watershed moment. It ends a long experiment in ultra-low rates and forces a reallocation of risk across savings, investment and currency strategies. For households, it is time to reassess borrowing plans and emergency buffers. For firms, balance-sheet management and interest-rate hedging become priorities. For investors, the new environment offers yield opportunities but also requires careful duration and currency management.

Tokyo stock market trading

- Japan's rate rise signals a significant policy shift with broad domestic and global consequences.

- Higher rates benefit savers and certain financial institutions but increase costs for borrowers and exporters.

- Market volatility is likely in FX and bond markets; clear central bank communication will be essential.

- Watch wage growth, inflation persistence and government debt servicing costs for clues about future policy.

The transition to higher rates is both an economic and social adjustment — understanding its winners, losers and transmission channels will be critical in the months ahead.