How Wall Street Uses Jargon to Justify Sky-High Fees

Wall Street financial district

The moment you step into a pitchbook, a conference room, or a quarterly investor memo, something happens: words start behaving less like tools for understanding and more like instruments of authority. Terms that sound technical and precise—alpha, liquidity transformation, synthetic exposure—act like a velvet curtain. Behind it, complex business models and large compensation pools are presented as inevitable, necessary, and even noble. This piece shows how language on Wall Street is deliberately shaped to protect revenue, blur accountability, and persuade clients that expensive services are worth every basis point.

Why Language Matters on Wall Street

Language is not neutral. In markets, it determines who belongs, who understands, and who can negotiate. Jargon performs three primary functions for financial firms: it signals expertise to prospective clients and recruits, it creates a boundary that discourages close questioning, and it reframes ordinary commercial choices as specialized, technical necessities.

Financial jargon terminology chart

Authority through Complexity

Complex vocabulary makes the speaker seem expert. When a fund manager uses a term like "portable alpha" or "liquidity overlay," listeners often assume there's a deep quantitative rationale behind it. The implicit promise is that the provider has access to intellectual capital that ordinary investors lack. In practice, that claim may be true, partially true, or entirely rhetorical—yet the language itself conveys credibility before any substance is examined.

Obfuscation as Negotiation Leverage

Jargon raises the cost of rigorous scrutiny. If understanding a fee requires a glossary, investors are less likely to dig into the math or push back during negotiations. That friction conserves the status quo: higher fees, more complex layers of compensation, and limited transparency. For sales teams, opacity is not a bug—it’s a feature.

Common Jargon—and What It Really Means

The following list translates the terms investors encounter so they can ask sharper questions and spot where words inflate the value proposition.

- Alpha: Literally, excess return over a benchmark. In marketing, it often refers to skill; in reality, it can reflect risk-taking, sector bets, or luck.

- Beta: Market exposure. Some firms use "beta" as shorthand for routine market risk to separate it from fee-bearing services.

- Liquidity Transformation: Taking short-term assets and presenting them as longer-term funding products, or vice versa. Customers may bear the liquidity risk despite paying for the manager's "services."

- Synthetic Exposure: Using derivatives to mimic an asset. It can reduce upfront capital needs but introduces counterparty and complexity risks.

- Alternative Beta: A marketing term that blurs inexpensive systematic exposures with expensive active management.

- Return Enhancement: A euphemism for strategies that increase volatility or add leverage to boost returns—often at a higher fee.

Investment fee structure breakdown

The Mechanics: How Jargon Inflates Earnings

Language interacts with compensation structures to create outsized profits. Consider three mechanisms: product layering, fee bifurcation, and performance accounting.

Product Layering

Firms bundle services into modular products: a core portfolio, a hedging overlay, a tail-risk solution, and an execution facility. Each layer comes with its own language and fee. When presented together, the total cost exceeds what a client might pay for a simpler, transparently priced arrangement. Because each layer is framed as a distinct, specialized service, clients often accept incremental charges rather than demand a consolidated, lower-cost alternative.

Fee Bifurcation and Rebranding

Fees are split into management, performance, admin, and platform charges, each given a name that makes it sound legitimate. "Platform fee" can cover distribution costs; "technology access" might refer to a client portal built at relatively low marginal cost. Splitting fees allows firms to advertise a modest headline rate ("only 0.75% management fee") while collecting additional streams that inflate net revenue.

Wall Street client presentation meeting

Performance Accounting

How returns are calculated—net or gross of fees, which benchmark is used, and what period qualifies for incentive payouts—matters a great deal. Complex definitions of "high-water marks," bespoke benchmarks, and look-back windows can accelerate performance fees even when absolute returns are mediocre. Jargon around these definitions keeps clients from easily comparing products.

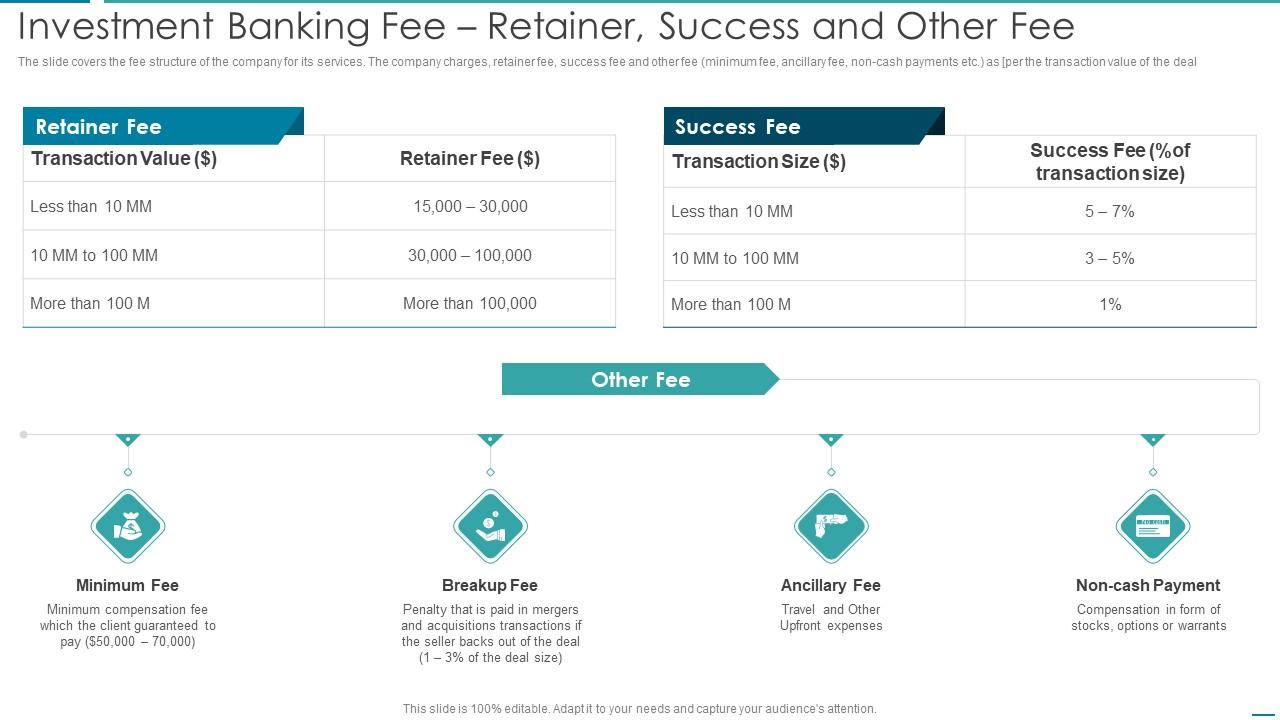

A Simple Table: How Fees Typically Appear

Below is a compact comparison to illustrate how a client sees multiple fee lines even when the product is functionally a single service.

| Fee Type | Typical Range | What the Client Actually Pays For |

|---|---|---|

| Management Fee | 0.5% – 2.0% | Portfolio construction and ongoing administration |

| Performance Fee / Carry | 10% – 30% of outperformance | Manager incentive; may reward risk-taking |

| Platform / Technology Fee | 0.05% – 0.50% | Client portal, reporting, and distribution |

| Transaction or Execution Fee | Variable | Trading costs; sometimes retained by the firm |

The Sales Playbook: From Pitch to Agreement

Sales on Wall Street follows a practiced choreography: initial discovery, a technical demonstration (the jargon-heavy segment), an appeal to track record, and a finalized agreement with complex terms. At every stage, language is tailored to reduce friction and increase perceived uniqueness.

The Technical Demonstration

This is where jargon shines brightest. A quant briefly explains a model using domain-specific terms, charts with dense annotations, and simulations that predict outperformance. Clients with imperfect time or technical expertise often take the presenter's word for the logic. The demonstration converts complexity into an aura of sophistication.

Financial regulation transparency documents

The Legal and Operational Layer

Contracts and subscription documents are another domain where specialized language serves the firm. Legalese and long-form exhibits hide small but significant provisions—fee cliffs, redemption windows, and side-pockets. Because reading and parsing these documents is time-consuming, many investors rely on advisors or glossaries rather than conduct their own line-by-line review.

Complex words don't just describe complexity; they create it—and once created, complexity helps firms hold onto profits.

When Jargon Crosses from Useful to Harmful

Jargon is not inherently malicious. Technical vocabulary enables specialists to communicate efficiently. It becomes harmful when it's used deliberately to obscure cost, shift risk, or protect high margins from scrutiny.

Retail and Institutional Consequences

Retail investors may pay for services whose incremental value is marginal. Institutional investors—pension funds, endowments—can also be victims when procurement processes rely on relationships or brand rather than transparent pricing. The consequences are real: reduced net returns for beneficiaries, misallocated capital, and eroded trust in financial institutions.

Investor protection plain language

How to Spot Jargon for What It Is

Investors can learn to see jargon as a signal to investigate, not a reason to defer. Here are practical checks you can apply immediately.

- Ask for the same number presented multiple ways: gross return, net return after all fees, and net return after estimated transaction costs.

- Request a plain-language fee summary that lists every charge the client may pay under three scenarios: average, strong, and poor performance.

- Demand clear benchmark definitions and ask why that benchmark matters for your goals.

- Insist on transparency around counterparties when derivatives or synthetic structures are used.

Regulation, Market Forces, and Plain-Language Initiatives

Policymakers and industry groups have long pushed for clearer disclosures and fiduciary duty standards. Market pressure also plays a role; as low-cost passive products proliferated, firms that relied purely on jargon had to either justify their premium or lose assets. Still, progress is uneven: innovative fee models coexist with highly opaque structures.

What Firms Say—And What They Mean

Firms will often claim that complexity is unavoidable because of the nuanced risks they manage. Sometimes that's true: certain strategies genuinely require sophisticated execution. Other times, complexity is a commercial choice: a product can be simplified but isn't because simplification would expose margins to competition.

A Checklist for Investors

Before signing any mandate or subscription agreement, run through this short checklist.

- Get the exact fee math in three scenarios.

- Ask for peer comparables—three similar strategies and their net returns.

- Request clarity on redemption terms and side pockets.

- Confirm who benefits from transaction and execution revenues.

- Insist on periodic plain-language reports, not just technical memos.

What Honest Communication Looks Like

Honest communication reframes jargon-filled claims into decisions and trade-offs: "We can increase expected return by X by taking Y type of risk, which you should accept only if you have a spare time horizon of Z years." That sentence holds the manager accountable for trade-offs instead of hiding them behind opaque terminology.

- Transparency builds trust and reduces negotiation friction over time.

- Short-term revenues may fall for firms that previously relied on opacity, prompting resistance.

Conclusion: Language Is Power—Use It

Wall Street's jargon has practical uses, but it has also been weaponized to protect margins and complicate accountability. For managers and salespeople, sophisticated language can be a legitimate shorthand for real complexity. For clients and allocators, however, that same language often hides costs and choices that materially affect outcomes.

Investors who insist on plain-language explanations, standardized fee disclosures, and repeated numerical examples will not only save money but also improve decision quality. Regulators and industry groups can nudge the market toward clarity, but demand from buyers is the most powerful force. Language is power—when investors use it as a tool for clarity rather than defer to it as a sign of expertise, the market becomes fairer.

Ask for the numbers. Ask for the assumptions. If the answer is elegant but vague, it probably serves someone else’s balance sheet more than it serves yours.

- Jargon signals expertise but can also be used to obscure fees and risks.

- Layered fees and bespoke performance accounting are primary mechanisms that inflate earnings.

- Demand plain-language fee breakdowns, multiple performance scenarios, and clear benchmarks before committing capital.

- Transparency benefits investors and markets; seller-side resistance often indicates a meaningful transfer of value.