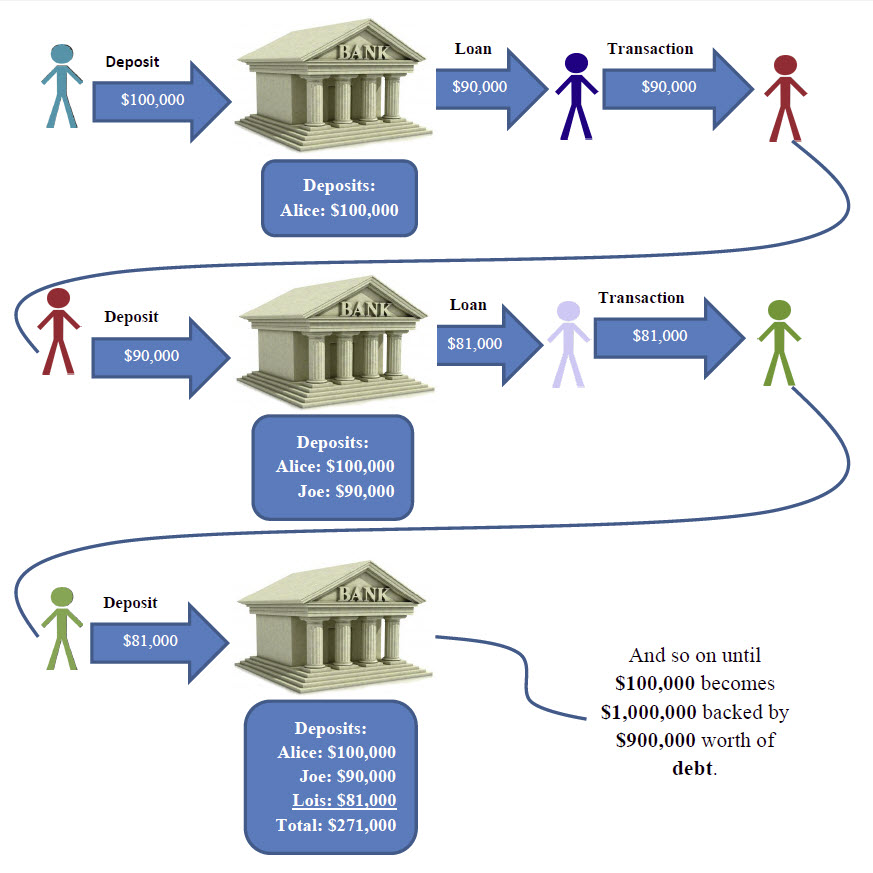

How Banks Create Money: Why Your $100 Can Exist Twice

Imagine you walk into your local bank and deposit a crisp $100 bill. Later that week a friend takes a $90 loan from the same bank to buy a bicycle. Suddenly, looking at account balances, it seems like there is $190 in the system: your $100 sitting in a deposit account and your friend’s $90 deposited by the seller. How can the same dollar be in two places at once? The short answer: because modern banking is bookkeeping that creates a new form of money—bank deposits—when banks lend. This article explains that process step by step, clears up common misconceptions, shows the limits and risks, and explains why this system matters for the economy.

bank balance sheet double entry

A Simple Walkthrough: The $100 Deposit and the $90 Loan

Start with two actors: you, the depositor, and Bank A. You hand over $100 in cash. The bank records two things on its balance sheet: an asset (the $100 in cash reserves it now holds) and a liability (a $100 deposit in your account). In double-entry accounting the bank’s books always balance: what it gets is an asset, what it promises is a liability.

Now the bank lends $90 to a borrower. It does not hand over the original $100 bill and write '$90' on a piece of paper. Instead it creates a new deposit in the borrower’s account for $90 and records a $90 loan as an asset on its books. The bank’s balance sheet expands: the loan is an asset; the borrower's deposit is a liability.

bank deposit creation process

When the borrower spends that $90, it typically ends up as a deposit at the same bank or another bank. If it goes to another bank, Bank A pays out reserves to that other bank; if it stays at Bank A, reserves are unchanged but deposits have shifted. Either way, we now have your original $100 deposit plus the new $90 deposit created when the bank made the loan. That is why it appears money was duplicated.

Why This Is Not Magical Double-Spending

The $90 loan is not the same physical dollar you deposited. Some important distinctions:

- Your $100 is a deposit liability of the bank: you can withdraw it or use it for payments.

- The $90 is also a deposit liability—but to a different customer. It represents a promise by the bank to transfer funds when instructed.

- The bank records a $90 loan asset that you don’t own; the borrower owes the bank that amount plus interest.

So money has not been copied in the literal sense. What has happened is the banking system created a new type of money—bank deposit credit—while simultaneously creating a corresponding debt. The new deposit increases the total amount of deposits in the economy, which is one commonly used measure of the money supply.

Balance Sheets: Where the Magic Lives

Understanding bank balance sheets is the clearest way to see why deposits can increase when banks lend. A simplified bank balance sheet:

- Assets: Reserves, loans, securities.

- Liabilities: Customer deposits, short-term borrowing.

- Equity: Capital provided by owners.

When a loan is made, both sides of the balance sheet increase by the loan amount: loans (assets) rise and deposits (liabilities) rise. The bank has created money in the form of new deposits, but it also has a new claim on the borrower. The net effect on the bank’s equity is nil at the moment of creation (ignoring fees and interest), because assets and liabilities rose equally.

fractional reserve banking diagram

Key Concepts: Assets, Liabilities, Reserves, and the Central Bank

Quick definitions that help keep the rest clear:

Reserves are crucial because they are how banks settle payments with one another and meet withdrawal requests. The central bank supplies reserves and acts as the lender of last resort if banks cannot get funds from the market. But reserves are not the same as the deposits people use for day-to-day transactions.

bank loan asset liability

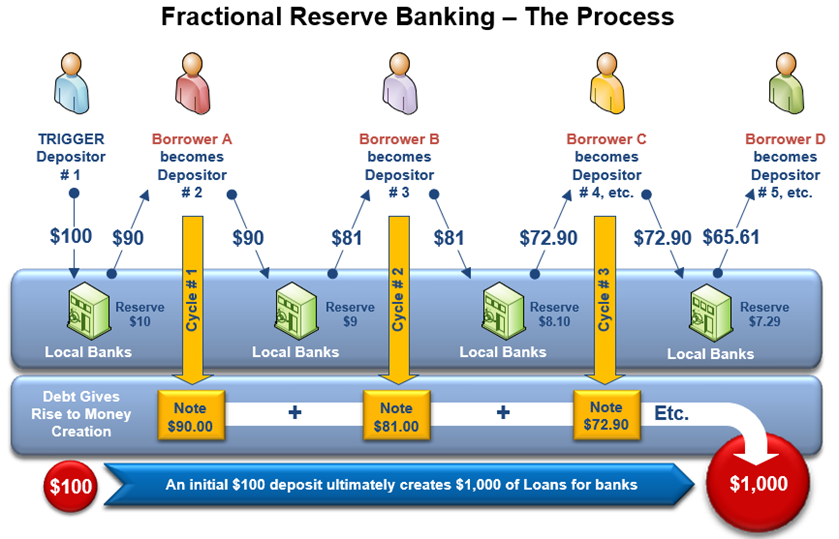

The Money Multiplier: A Useful but Simplified Picture

Textbook explanations often use a money multiplier model: if banks keep 10% of deposits as reserves (a reserve ratio of 10%), then the theoretical maximum expansion of deposits from an initial $100 base is 1 / 0.10 = 10 times, giving $1,000 in deposits. That model shows why your $100 could support more lending in the economy.

But modern banking is more complex. The simple multiplier assumes banks lend until they hit a reserve constraint and that all loaned funds are redeposited within the banking system and not held as cash. In reality, lending is shaped by borrower demand, credit standards, capital requirements, profitability, and the central bank’s policy rate. Reserves are not always the binding constraint.

money multiplier textbook model

Who Sets the Limits? From Reserve Ratios to Capital Rules

Two institutional limits prevent unlimited money creation.

1) Reserve and Liquidity Needs

Banks must manage liquidity to meet deposit withdrawals and payments. If a bank sees heavy outflows, it needs reserves or cash to settle. Central banks can supply reserves, but short-term liquidity stress can be disruptive.

2) Capital Requirements and Risk Management

Banks must hold capital—equity and certain retained earnings—against risky assets like loans. Capital is the cushion that absorbs losses. Regulators set minimum capital ratios (for example under international Basel rules) that limit how much a bank can expand lending relative to its capital. So even if reserves are plentiful, a bank cannot lend endlessly without more capital or lower risk-weights.

central bank reserves system

Is New Money 'Real' Money? The Difference Between Gross and Net

It's helpful to distinguish between gross money (the total of deposits) and net financial wealth. When a bank creates a $90 deposit and a $90 loan, aggregate deposits rise, which increases gross money supply. But the borrower also has a $90 liability to the bank. For the private sector as a whole, that newly created deposit is offset by the newly created debt—net financial assets across the private sector may not have risen by the loan amount.

However, for the person who deposited $100, the new $90 deposit is additional liquidity they can use to buy goods and services. That increased liquidity matters for spending and economic activity, even if the private sector’s net financial position remains balanced between assets and debts.

A Few Practical Examples

Example 1: All within one bank. You deposit $100 at Bank A. Bank A lends $90 to a borrower whose seller also banks with Bank A. The $90 is paid into the seller’s deposit at Bank A. Reserves stay the same, but deposits increased to $190. Bank A has more loans and more deposits. Money supply (deposits) rises.

Example 2: Borrower’s spending goes to another bank. You deposit $100 at Bank A. Bank A lends $90 and the seller banks at Bank B. Bank A transfers $90 in reserves to Bank B. Bank A’s reserves fall by $90 (from your $100) and it now holds a $90 loan asset; Bank B’s reserves increase by $90 and its deposits increase by $90. The banking system’s aggregate deposits still rose by $90 overall.

Common Misconceptions

Misconception: The bank simply hands out existing depositors’ money when lending. Not true — lending creates a deposit, it doesn’t usually take one deposit to fund another.

Misconception: Banks are free to create unlimited money. Not true. Capital requirements, profitability, borrower creditworthiness, and regulatory oversight all limit lending.

Misconception: Created deposits are worthless because they are offset by debt. While debt exists, created deposits function as money for transactions and change the composition of financial assets and liabilities—this drives consumption, investment, and prices.

bank run scenario warning

Policy Tools and Broader Implications

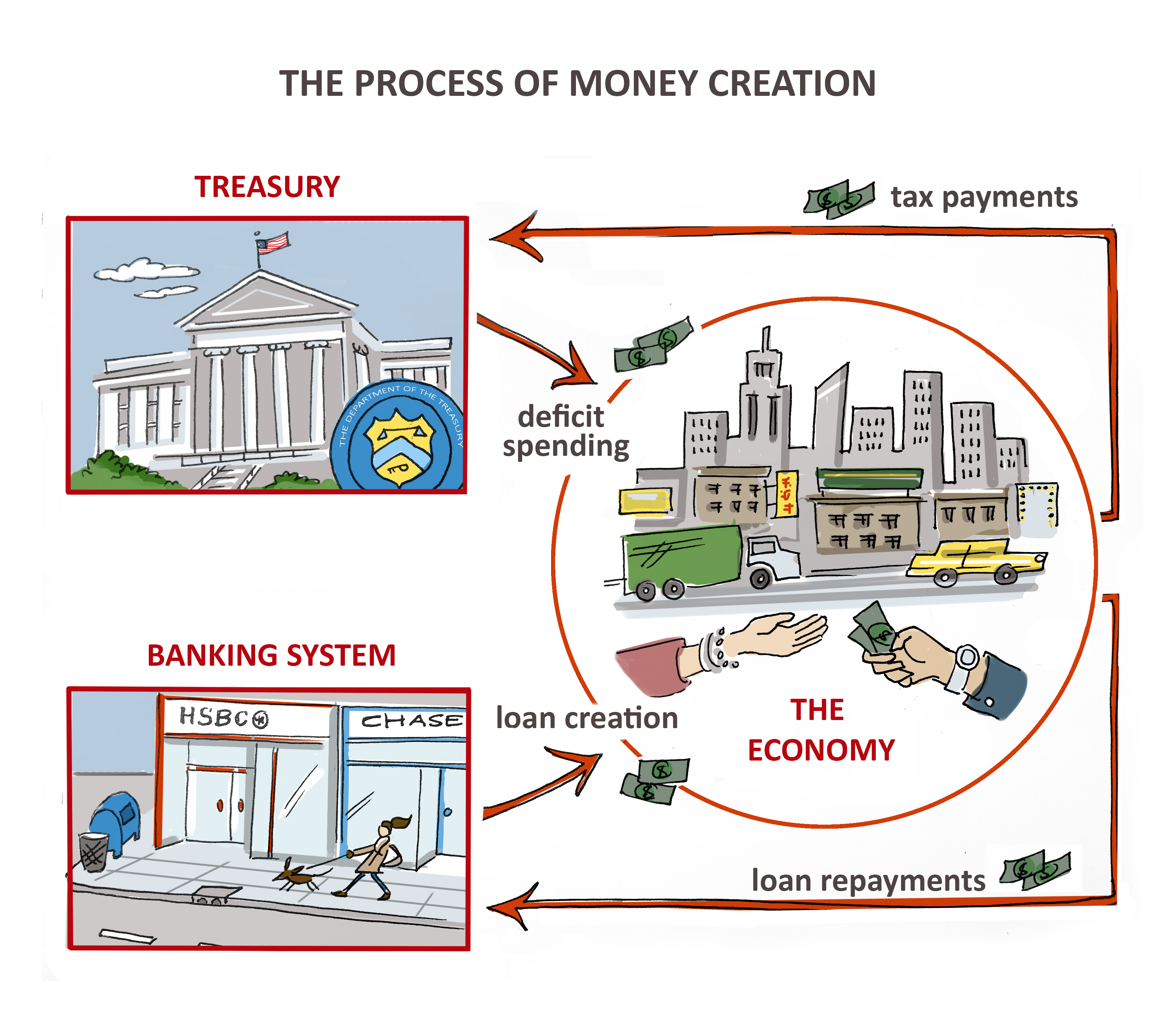

Central banks influence money creation indirectly. By setting interest rates and supplying reserves, they affect the cost of bank funding and the overall demand for loans. Fiscal policy (government spending and taxation) also affects borrowing demand and the banking system’s willingness to lend.

During booms, extensive credit creation can inflate asset prices and lead to financial instability. During busts, banks pull back on lending, which can shrink deposits and deepen recessions. That asymmetry is why macroprudential tools and countercyclical capital buffers are now common policy features in many jurisdictions.

The Payment System: How Bank Money Works in Practice

Most purchases in modern economies are settled by transferring bank deposits, not cash. When you pay with a debit card, your bank debits your deposit and credits the merchant’s bank through the interbank settlement system. The central bank’s reserve accounts are used to settle between banks, but everyday transactions use deposit balances.

What Happens When Loans Are Repaid or Default?

Repayment: When a borrower repays principal, the bank reduces the loan asset and reduces the depositor’s account (or uses reserves) to record the repayment. Repayment destroys the deposit money created when the loan was issued—the bank’s balance sheet shrinks.

Default: If a borrower defaults, the bank still has the deposit liability outstanding but suffers a loss on its asset side. Losses reduce bank capital and can force reductions in lending or need for recapitalization. That is why banks assess credit risk carefully and hold capital to absorb losses.

Why This Matters to You

Understanding how banks create money helps make sense of inflation, why interest rates matter, and how economic policy affects credit and housing prices. It explains why saving in deposits can be safe (insured) while lending generates broader economic activity—and why too much credit expansion can be risky.

lending creates deposit money

Key Takeaways

- Commercial banks create deposit money when they make loans; the loan is the matching asset that keeps balance sheets in equilibrium.

- Deposits can appear to exist in two places because lending creates new deposits while the original deposit remains a bank liability.

- Limits on money creation include capital requirements, liquidity needs, borrower demand, and regulatory oversight—not just reserve ratios.

- Repayment of loans destroys deposits; defaults erode bank capital and can reduce lending.

- Bank-created deposits are real money for transactions and have meaningful effects on spending and prices.

'Bank deposits are promises that power the payments system—lending creates the promise, and the promise becomes money.'

Final Thoughts

The idea that $100 can 'exist twice' is at once a bookkeeping reality and an intuitive puzzle. It arises because modern money mixes legal tender, bank promises, and contractual debt. Banks do not perform a literal act of duplication; they create liabilities (deposits) and matching assets (loans) through accounting entries. That creation expands the money available for spending, investment, and growth—but it also creates obligations and risks that regulators and markets must manage. Understanding this system makes you a savvier consumer of economic news and policy debates, and it clarifies why central banks and governments watch credit growth so closely.

- Facilitates economic activity by turning savings into loans.

- Expands the supply of transactional money efficiently.

- Can inflate asset bubbles if credit expands too fast.

- Creates systemic risk if losses erode bank capital.

Questions about money creation can feel abstract, but they matter in everyday life: from mortgage rates and job creation to the safety of bank accounts and the direction of economic policy. Next time you deposit cash or hear about bank lending, remember: what looks like duplication is actually the banking system doing what it was designed to do—create credit, support transactions, and help allocate resources across the economy.