Europe's Pension Reckoning: How Young People Paid the Price

The story of modern Europe is, in many ways, a story about promises: promises that pensions would be there at the end of a working life, promises of dignity in old age, promises that economies could grow while the state insured the vulnerable. Over the last few decades those promises ran into a stubborn demographic reality and a global financial shock, and the political answer in many countries has been to push the cost of adjustment onto those least able to pay—the young. This feature traces how routine policy choices, fiscal emergencies and market reforms translated into higher risk, lower security and diminished prospects for a generation.

The Problem: Aging and Promises

Demographic shift

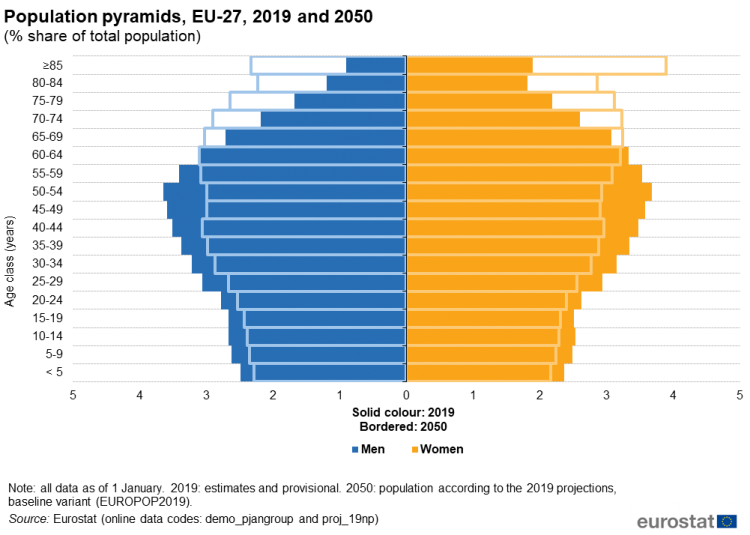

Europe's population is older than most other regions: births per woman have fallen for decades and life expectancy has generally risen. That combination creates a longer retirement period paid by a relatively smaller working population. The arithmetic is simple: pay-as-you-go pension systems rely on current workers to fund current retirees. As the ratio between workers and pensioners falls, either contributions must rise, benefits must fall, or the system must be supplemented by borrowing or private savings. All of those adjustments have distributional consequences—who bears the cost, now and in the future?

Europe demographic aging population

Promises and political economy

Pensions are political capital. Governments offered generous guarantees because they are visible, immediate benefits for aging voters—the very group that turns out in higher numbers at the ballot box. The short-term politics often outweighed the long-term fiscal logic. Over decades small changes compounded into large unfunded liabilities, sometimes hidden in accounting rules or managed by ad hoc indexing. When a financial crisis hit, or growth slowed, the pressure to rebalance budgets made pensions a target for reform.

Policy Responses: Cuts, Delays, and Marketization

Raising the retirement age and reducing generosity

One of the most visible policy responses has been to raise statutory retirement ages and tighten eligibility rules. Policymakers argued that longer life expectancies justified later retirement and that delaying benefits would reduce the strain on public finances. While conceptually defensible, in practice these changes often failed to account for unequal lifespans across socio-economic groups or the reality of physically demanding jobs. For workers in precarious sectors or with lower life expectancy, the relative loss can be large.

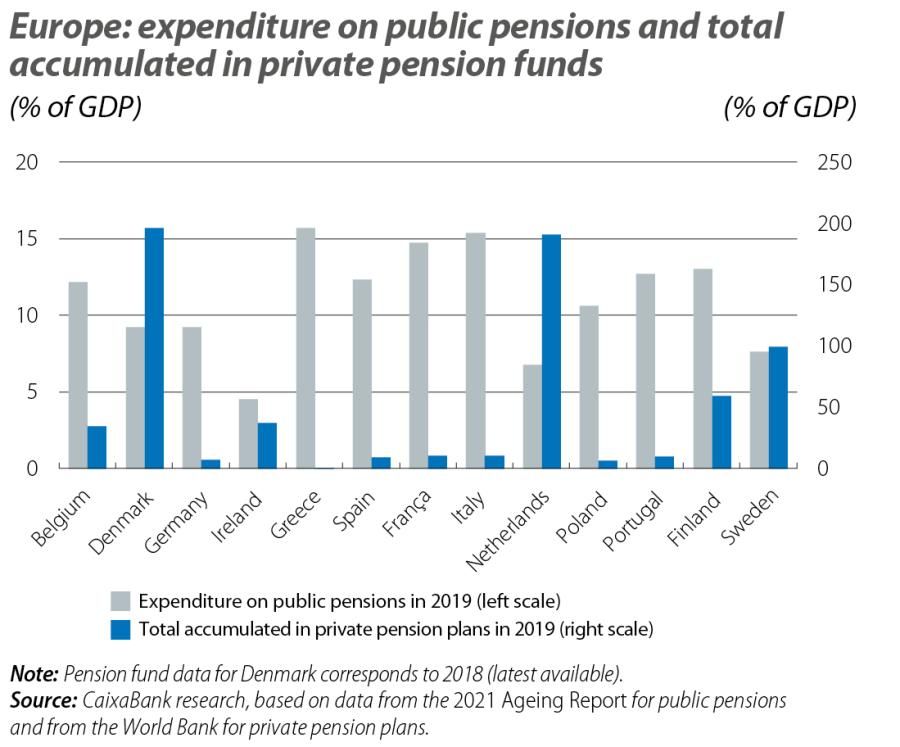

From defined benefit to defined contribution

A second trend has been the gradual shift from defined benefit systems—where the state guarantees a formulaic payment—that transfer risk to individuals. Privatization and private pensions were sold as a way to reduce state liabilities and encourage savings. But private markets expose retirement incomes to volatility, fees and inadequate returns. For young people already facing precarious employment and low wages, mandated private contributions often feel like an extra tax that buys less security than promised.

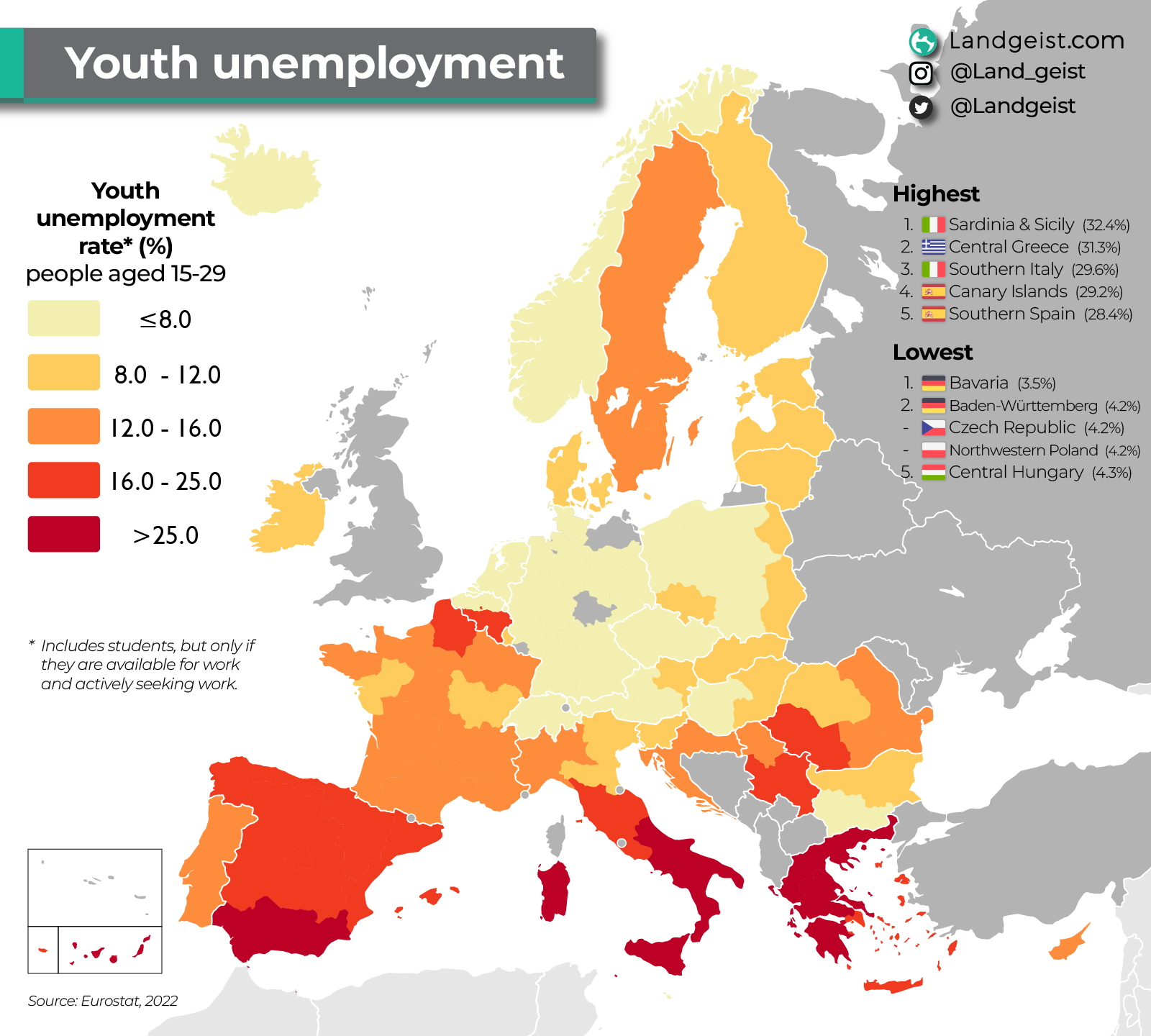

Youth unemployment Europe

Austerity and fiscal reallocation

Following financial and sovereign debt crises, austerity policies in several countries prioritized deficit reduction over public investment or redistribution. Reforms cut back on pension indexation, benefits and, in some places, introduced means-testing or targeted reductions. The result was a narrow fiscal victory—short- to medium-term savings—but a political and social cost: young cohorts suddenly faced a future with lower expected public transfers while being asked to shoulder higher contributions and longer working lives.

European pension reform austerity

How Young People Bore the Burden

Labor-market scarring and delayed careers

Young people entered the workforce at moments of weak job creation in many European countries. High youth unemployment, informal work and a rise in temporary contracts didn't just limit incomes in the present; it reduced contributions to pension systems and created 'scarring'—lasting damage to earnings trajectories. Lower lifetime earnings translate to lower pension entitlements in many systems, meaning today's structural unemployment becomes tomorrow's under-pensioned elderly.

Taxation and contributions

To stabilize pension schemes, governments often raised payroll taxes or shifted more of the burden onto workers through higher mandatory contributions to private schemes. For a young person just starting a family or trying to save for housing, these design changes reduce disposable income and squeeze the capacity to build private buffers. Additionally, when contributions finance current retirees rather than being saved, a generation of workers effectively subsidizes older cohorts for present consumption at the expense of their future security.

Housing and savings gap

Across Europe, housing prices in major cities soared relative to wages. Young people who might once have relied on home equity to smooth retirement are now entering middle age with little or no property wealth. Without that traditional buffer, the loss of expected public pensions or weaker private returns becomes more acute. The combination of expensive housing, persistent rent burdens and prolonged inability to save means reduced resilience in old age.

Education, debt and delays

Higher education expanded across Europe over recent generations, but it often came with higher costs and delayed labor market entry. Student debt, professional internships and long apprenticeships compress the period of peak earnings. Longer training and earlier precariousness together reduce cumulative contributions and exacerbate the transfer of pension burden to younger cohorts.

The policy choices that look technical on paper—indexation rules, contribution rates, retirement ages—translate into life-defining shifts for entire generations.

Pension privatization Europe

Political and Social Consequences

Erosion of trust and the social contract

Pensions sit at the heart of the social contract: a compact between work, state and citizenship. When that compact feels broken—when younger people perceive that their labor finances someone else's comfort while their own future is less secure—trust in institutions diminishes. This erosion manifests politically as lower turnout among younger voters, rising support for populist movements, or growing intergenerational tensions in public discourse.

Economic growth and productivity

Long-term growth can be affected when youth face constrained consumption, limited ability to invest in skills, or delayed family formation. Reduced demand and a less dynamic labor force feed back into fiscal pressures, creating a cycle that makes future pension promises even harder to meet. In other words, shifting costs onto young people can shrink the very economic base needed to sustain retirement systems.

Intergenerational equity Europe

Case Studies in Policy Choices

Northern consolidation and Southern shocks

Different European economies responded differently. Some northern systems combined active labor policies with gradual reforms and diversified funding, while in parts of southern Europe sharp fiscal consolidation after debt crises produced abrupt cuts and longer-lasting youth unemployment. These divergent paths underscore that outcomes are not inevitable; policy design and the timing of reforms matter deeply.

Market-based experiments and social fallout

Where private pension markets expanded aggressively, administrative costs, poor regulation and concentration of providers often meant the promised benefits underdelivered. Market failures and weak financial literacy left many young contributors with diminished returns—another way in which risk was quietly exported from the state to individuals ill-equipped to manage it.

Alternatives and What Could Be Done Differently

Redistribute across wealth, not just age

A central idea is to broaden responsibility for pension funding beyond the narrow worker-retiree axis. Wealth taxes, higher income taxes on the highest earners, or closing tax expenditures can shift the burden away from young wage-earners and toward those with greater capacity to pay. Such measures are politically contentious, but they target inequality rather than generational conflict.

Hybrid models and risk sharing

Instead of fully privatizing risk or leaving all adjustments to future workers, hybrid models combine a basic universal safety net with earnings-related components that share demographic risks across cohorts. Risk-sharing mechanisms—such as smoothing buffers, longevity adjustment formulas that treat cohorts more equitably, or government-backed minimum floors—can preserve dignity without exposing young people to unmanageable burdens.

- Targeted redistribution can protect vulnerable young workers.

- Hybrid schemes lower volatility of retirement income.

- Political resistance to higher taxes on wealth and income.

- Implementation complexity when overhauling entrenched systems.

Invest in youth employment and lifetime earnings

Perhaps the most sustainable route is to invest in policies that increase lifetime earnings: early-childhood care to boost labor participation, active labor-market programs that reduce long-term unemployment, incentives for stable contracts, and targeted training that responds to technological change. Raising the denominator—the number of contributors and their average earnings—eases pressure without cutting benefits dramatically.

Reclaiming public narratives

Finally, policymakers must be honest and transparent about trade-offs. Framing reforms as technical tinkering hides distributional stakes. Open debate about who pays, how benefits are calculated and what public pensions are meant to guarantee builds legitimacy and can reduce generational resentment.

Practical Steps for Young People Navigating the System

Active engagement and planning

Young people can respond at two levels: individually and collectively. Individually, building financial literacy, prioritizing emergency savings, and understanding employer pension schemes reduces vulnerability. Collectively, political engagement and advocacy for fair policy designs—campaigning for stronger youth employment measures, progressive taxation or pension floors—shifts the balance of power in policy debates.

Conclusion: A New Social Compact for Retirement

The gradual transfer of pension risk onto young people was not the product of a single decision or villain but of many smaller choices—technical reforms, fiscal emergencies, market enthusiasm and political calculations—that collectively shifted costs across generations. Fixing this requires more than tweaking contribution rates: it demands a reimagining of the social contract that recognizes demographic realities while protecting the future of those who must work longer to pay for earlier promises.

There are no easy answers, but there are clearer choices. Policymakers can prioritize growth strategies that broaden the tax base, redesign systems to share risk fairly, and tax wealth where it accumulates. Young people and their advocates can insist on reforms that do not lock them into a lifetime of weaker retirement security. The question facing Europe is whether it will accept a fractured social compact or work toward a system that restores trust and spreads burdens in ways that are seen as legitimate and fair.

- Pension strain in Europe is driven by demographic change and political choices, not inevitability.

- Shifting from public guarantees to private risk has transferred costs to younger generations with precarious labor-market positions.

- Alternatives exist: progressive taxation, hybrid risk-sharing schemes, and active labor-market policies that raise lifetime earnings.

- Repairing trust requires honest public debate and policy designs that prioritize intergenerational fairness.